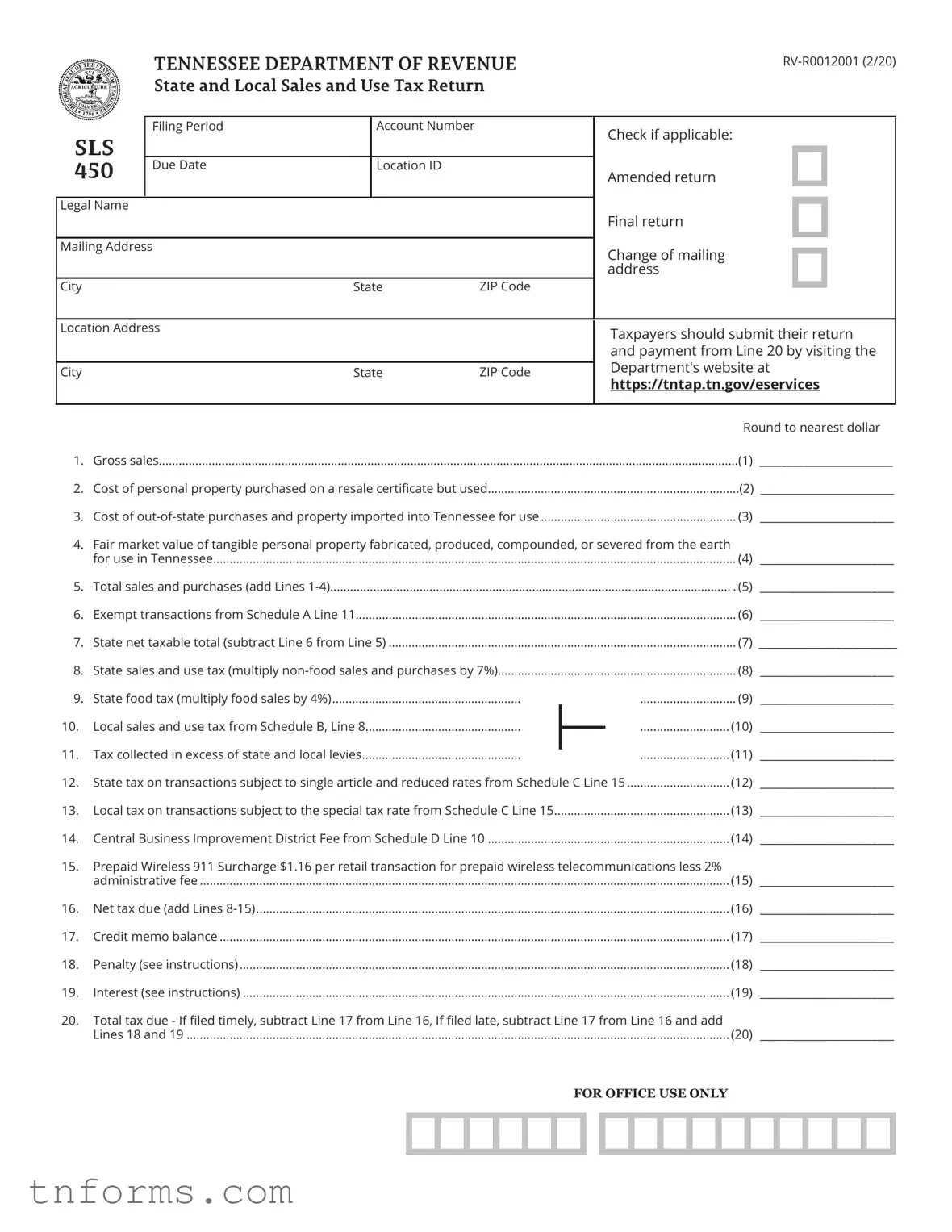

Fill Out a Valid 450 Tennessee Form

In the nuanced landscape of Tennessee's tax obligations, the importance of the 450 Tennessee form, administered by the Tennessee Department of Revenue, cannot be overstated. This form, also known as the State and Local Sales and Use Tax Return, is a critical tool for businesses to report their gross sales, taxable and exempt transactions, and calculate due taxes, including special considerations such as the Central Business Improvement District Fee and the Prepaid Wireless 911 Surcharge. Notably, the form caters to various adjustments and exemptions, underscoring the state's recognition of the complex nature of business operations. It requires detailed inputs ranging from gross sales to specific deductions for items like sales to government or qualified nonprofit institutions and sales made during the Sales Tax Holiday. Additionally, this form reflects Tennessee's adaptability to e-commerce and out-of-state sellers with instructions for reporting sales by the destination, emphasizing the evolving tax landscape. Its comprehensive structure ensures that businesses accurately fulfill their tax liabilities, making it an indispensable part of Tennessee's fiscal framework.

Example - 450 Tennessee Form

TENNESSEE DEPARTMENT OF REVENUE |

|

STATE AND LOCAL SALES AND USE TAX RETURN |

|

|

Filing Period |

|

Account Number |

|

SLS |

|

|

|

|

450 |

Due Date |

|

Location ID |

|

|

|

|

|

|

Legal Name |

|

|

|

|

|

|

|

|

|

Mailing Address |

|

|

|

|

|

|

|

|

|

City |

|

State |

ZIP Code |

|

|

|

|

|

|

Check if applicable:

Amended return

Final return

Change of mailing address

Location Address

City |

State |

ZIP Code |

Taxpayers should submit their return and payment from Line 20 by visiting the Department's website at

https://tntap.tn.gov/eservices

|

|

|

|

Round to nearest dollar |

|

1. |

Gross sales |

(1) |

________________________ |

||

2. |

Cost of personal property purchased on a resale certificate but used |

(2) ________________________ |

|||

3. |

Cost of |

(3) |

________________________ |

||

4. |

Fair market value of tangible personal property fabricated, produced, compounded, or severed from the earth |

|

|

||

|

for use in Tennessee |

(4) |

________________________ |

||

5. |

Total sales and purchases (add Lines |

. (5) |

________________________ |

||

6. |

Exempt transactions from Schedule A Line 11 |

(6) |

________________________ |

||

7. |

State net taxable total (subtract Line 6 from Line 5) |

(7) |

_________________________ |

||

8. |

State sales and use tax (multiply |

(8) |

________________________ |

||

9. |

State food tax (multiply food sales by 4%) |

(9) |

________________________ |

||

10. |

Local sales and use tax from Schedule B, Line 8 |

|

|

(10) |

________________________ |

|

|

||||

|

|

||||

11. |

|

|

|

(11) |

________________________ |

Tax collected in excess of state and local levies |

|||||

12. |

State tax on transactions subject to single article and reduced rates from Schedule C Line 15 |

(12) |

________________________ |

||

13. |

Local tax on transactions subject to the special tax rate from Schedule C Line 15 |

(13) |

________________________ |

||

14. |

Central Business Improvement District Fee from Schedule D Line 10 |

(14) |

________________________ |

||

15.Prepaid Wireless 911 Surcharge $1.16 per retail transaction for prepaid wireless telecommunications less 2%

|

administrative fee |

(15) |

________________________ |

16. |

Net tax due (add Lines |

(16) |

________________________ |

17. |

Credit memo balance |

(17) |

________________________ |

18. |

Penalty (see instructions) |

(18) |

________________________ |

19. |

Interest (see instructions) |

(19) |

________________________ |

20.Total tax due - If filed timely, subtract Line 17 from Line 16, If filed late, subtract Line 17 from Line 16 and add

Lines 18 and 19 |

(20) ________________________ |

FOR OFFICE USE ONLY

Schedule A- Exempt Transactions (See Separate Instructions)

1. |

Net taxable food sales |

(1) |

____________________ |

2. |

Sales made to vendors or other establishments for resale, and sales of items to be used in processing |

|

|

|

articles for sale. (Certificates of Resale required) |

(2) |

____________________ |

3. |

Sales of items paid for with SNAP Benefits |

(3) |

____________________ |

4. |

Sales to federal or Tennessee governments and qualified nonprofit institutions (Certificate required) |

(4) |

____________________ |

5. |

Returned merchandise reported as sales on this or a previous return. Show on Schedule B, Line 2 |

|

|

|

amounts claimed on Schedule B, Line 4, of prior returns |

(5) |

____________________ |

6. |

Exempt industrial machinery and agricultural purchases |

(6) |

____________________ |

7. |

Sales in interstate commerce |

(7) |

____________________ |

8. |

Repossessions - portion of unpaid principal balances in excess of $500 due on TPP repossessed from |

|

|

|

customers. Report same amount on Schedule B, Line 2 |

(8) |

____________________ |

9. |

Other deductions (See instructions) |

(9) |

____________________ |

10. Sales Tax Holiday (last Friday in July through following Sunday) |

(10) ____________________ |

||

11. Total exemptions (Add Lines 1 through 10; enter here and on First Page, Line 6) |

(11) ____________________ |

||

Attention Sellers located outside Tennessee:

Beginning October 1, 2019, all sales that originate from a business located outside of Tennessee and sold to a destination inside Tennessee must be reported using the tax rate applicable to the delivery destination. Report all your sales made by location using Schedule E and bring total of all sales from Columns C through J over to Lines 1 through 8 below.

Schedule B - Local Sales and Use Tax (See Separate Instructions)

1. |

State net taxable total from First Page, Line 7 |

(1) |

____________________ |

2. |

Adjustments (total of Schedule A, Line 1 and any applicable amounts from Schedule A, Lines 5 and 8) |

(2) |

____________________ |

3. |

Total with adjustments (add Lines 1 and 2) |

(3) |

____________________ |

4. |

Excess amount over single article tax base |

(4) |

____________________ |

5. |

Energy fuel sales taxed at full state rate |

(5) |

____________________ |

6. |

Other deductions including sales of specified digital products and of merchandise sold through vending machines (6) ____________________ |

||

7. |

Net taxable total (subtract Lines 4, 5, and 6 from Line 3) |

(7) |

____________________ |

8. |

Local sales and use tax (multiply Line 7 x the applicable local tax rate; Enter here and on the first page, Line 10).... |

(8) |

____________________ |

Schedule C - State Single Article Tax and Special Tax Rates (See Separate Instructions) If no taxable single articles were sold at $1,600 or above, or if you have no special tax rate products to report, put $0 on Lines 9 and 15 below

and on Lines 12 and 13 on the first page.

1. |

Taxable single article sales from $1,600 to $3,200 |

(1) |

___________________ |

2. |

State single article sales tax (multiply Line 1 x 2.75%) |

(2) |

___________________ |

3. |

Industrial water sales |

(3) |

___________________ |

4. |

Industrial water tax (multiply Line 3 x 1.00%) |

(4) |

___________________ |

5. Industrial energy fuel sales |

(5) |

___________________ |

|

6. |

Industrial energy fuels tax (multiply Line 5 x 1.50%) |

(6) |

___________________ |

7. |

Aviation fuel tax (total amounts from Lines A and B; multiply x 4.50%) |

(7) ____________________ |

|

A.Taxable aviation fuel sales ($__________) Gallons (__________)

B.

8. Water carrier energy fuel tax (total amounts from Lines A and B; multiply x 7.00%) |

|

|

(8) ____________________ |

|||

|

A. Taxable energy fuel sales to water carriers ($__________) Gallons (__________) |

|

|

|

||

|

|

|

|

|||

|

B. |

|

|

|

|

|

|

|

|

|

|

||

9. State single article and reduced rates tax (Add Lines 2, 4, 6, 7, and 8) |

|

|

(9)___________________ |

|||

|

|

|||||

|

Enter here and on Line 12 on the first page |

|

|

|

||

10. Local industrial water tax (multiply total sales x 0.50%) |

|

|

(10) __________________ |

|||

11. Specified digital products sales |

|

|

(11) __________________ |

|||

12. Specified digital products local tax (multiply Line 11 x 2.50%) |

|

|

(12) __________________ |

|||

13. Sales of merchandise through vending machines |

|

|

(13) __________________ |

|||

14. Local tax on merchandise sold through vending machines (Multiply Line 13 x 2.25%) |

|

|

(14) __________________ |

|||

15. Total local special rates tax (Add Lines 10, 12, and 14). Enter here and on Line 13 on the first page |

(15) __________________ |

|||||

|

Schedule D- Central Business Improvement District (CBID) Schedule |

|

|

|

||

1. |

Gross sales less exempt transactions (Page 1, Line 1 minus Line 6) plus net taxable food sales |

|

|

|

||

|

(Schedule A, Line 1) |

|

|

(1) ___________________ |

||

2 . Sales of professional services included in Line 1 above |

|

|

(2) ___________________ |

|||

3. |

Sales of lodging provided to transients not included in exempt transactions |

|

|

(3) ___________________ |

||

4. |

Sales of tickets to sporting events or other live ticketed events not included in exempt transactions |

(4) ___________________ |

||||

5. |

Sales of alcoholic beverages subject to LBD tax not included in exempt transactions |

|

|

(5) ___________________ |

||

6. |

Sales of newspapers and other publications not included in exempt transactions |

|

|

(6) ___________________ |

||

7. |

Sales of overnight and |

|

|

(7) ___________________ |

||

8. |

Total CBID Exempt Sales - add Lines 2 - 7 |

|

|

(8) ___________________ |

||

9. |

Net Sales - subtract Line 8 from Line 1 |

|

|

(9) ___________________ |

||

10. Central Business Improvement District Fee - multiply Line 9 x 0.25%. Enter here and on page 1, Line 14 |

(10)___________________ |

|||||

|

|

|

||||

|

|

Under penalties of perjury, I declare that I have examined this report, and to the best of my knowledge and belief, |

||||

|

|

it is true, correct, and complete. |

|

|

|

|

|

|

____________________________________________________ |

_____________________ __________________________________________ |

|||

|

|

Taxpayer's Signature |

Date |

Title |

|

|

|

|

____________________________________________________ |

_____________________ ________________ |

________________________ |

||

|

|

Tax Preparer's Signature |

Preparer's PTIN |

Date |

Telephone |

|

|

|

____________________________________________________ |

____________________________ ________ |

________________________ |

||

|

|

Preparer's Address |

City |

|

State |

ZIP Code |

|

|

Preparer's Email Address____________________________________________________________________________________________ |

||||

|

|

|

|

|

|

|

Schedule E - For Sellers Located Outside Tennessee Destination Sales Report

A |

B |

C |

D |

E |

F |

|

G |

|

H |

|

I |

|

J |

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or County |

Sales Tax |

State Net |

Adjustments |

Adjusted |

Excess of |

|

Energy Fuel |

|

Other |

|

Local Net |

|

|

Location |

Holiday |

Taxable Total |

Total |

Single Article |

|

Sales |

|

Deductions |

|

Taxable Total |

|

Local Tax |

|

|

|

|

|

|

Tax Base |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Totals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: If you have additional entries to report, please add additional Schedules as needed. Report total of all sheets on last page.

Form Breakdown

| Fact Name | Detail |

|---|---|

| Form Designation | The form is identified as the Tennessee Department of Revenue Form SLS 450. |

| Purpose | It serves for reporting State and Local Sales and Use Tax. |

| Submission Method | Submission of the return and payment from Line 20 is conducted through the Department's website. |

| Special Features | Offers options for amended returns, final returns, and change of mailing address. |

| Governing Law | Regulated under Tennessee sales and use tax laws. |

Detailed Instructions for Filling Out 450 Tennessee

Filling out the Tennessee Department of Revenue's Sales and Use Tax Return, known as the 450 form, might seem daunting, but by breaking it down step by step, this essential task can be tackled with confidence. Once completed, this form plays a crucial role in compliance with state tax obligations, ensuring that businesses contribute their fair share to the development and maintenance of state and local resources. To achieve accuracy and avoid common pitfalls, follow the detailed instructions below.

- Start by entering the filing period and account number at the top of the form.

- Fill in the due date, location ID, legal name, and mailing address including city, state, and ZIP code.

- If applicable, mark the boxes for an amended return, final return, or change of mailing address.

- Provide the location address if different from the mailing address, including city, state, and ZIP code.

- For line 1, report your gross sales.

- Next, for line 2, enter the cost of personal property purchased on a resale certificate but used by your business.

- In line 3, include the cost of out-of-state purchases and property imported into Tennessee for use.

- Line 4 asks for the fair market value of tangible personal property fabricated, produced, compounded, or severed from the earth for use in Tennessee.

- Add lines 1-4 to calculate your total sales and purchases, entering this sum in line 5.

- Line 6 requires you to input exempt transactions from Schedule A Line 11.

- Subtract line 6 from line 5 to find the state net taxable total, and enter this figure in line 7.

- Calculate and enter your state sales and use tax for non-food sales in line 8 by multiplying the state net taxable total by 7%.

- For line 9, compute the state food tax by multiplying food sales by 4%.

- Refer to Schedule B, Line 8, for the local sales and use tax, and transcribe this amount to line 10.

- In line 11, document any tax collected in excess of state and local levies.

- Find the state tax on transactions subject to single article and reduced rates from Schedule C Line 15 and fill in line 12.

- The local tax on transactions with special tax rates from Schedule C Line 15 should be reported on line 13.

- For the Central Business Improvement District Fee from Schedule D Line 10, report this amount on line 14.

- Document the Prepaid Wireless 911 Surcharge in line 15, inclusive of the $1.16 charge per retail transaction for prepaid wireless telecommunications, subtracting a 2% administrative fee.

- Add lines 8 through 15 to estimate your net tax due and enter this sum on line 16.

- If you have a credit memo balance, input this amount in line 17.

- Line 18 is for any penalty as indicated in the instructions, followed by line 19 for interest. Calculate these as necessary.

- To find the total tax due, subtract line 17 from line 16 if filed on time. If late, add lines 18 and 19 to the result and enter this figure in line 20.

- The section for office use only should be left blank.

- Complete the schedules A through E as they apply to your transactions, referencing each relevant set of instructions for accuracy.

- Make sure to sign and date the form, also providing the title, and if completed with assistance, have the tax preparer sign and include their details as well.

Once you have meticulously filled out the form and reviewed all the details for correctness, you're ready to submit it along with any payment due by visiting the Tennessee Department of Revenue's website. Remember, accuracy and timeliness are key to ensuring that your business remains in good standing and contributes to the state's economic strength.

More About 450 Tennessee

Frequently Asked Questions about the 450 Tennessee Form

What is the 450 Tennessee Form used for?

The 450 Tennessee Form is a document designed for businesses to report and pay state and local sales and use taxes in Tennessee. This form helps businesses calculate their tax responsibilities based on their gross sales, purchased goods, and other taxable activities.

How do I submit the 450 Tennessee Form?

Businesses can submit the 450 Tennessee Form and the associated payment through the Tennessee Department of Revenue's website. Detailed instructions are provided on the form to ensure accurate submission. Simply go to https://tntap.tn.gov/eservices and follow the instructions for submission.

What should I do if I need to amend a previously filed 450 Tennessee Form?

If you need to amend a previously filed 450 Tennessee Form, you should mark the "Amended return" box on the form. Provide the updated information to correct any errors or omissions in your original submission.

When is the 450 Tennessee Form due?

The due date for the 450 Tennessee Form is indicated on the form itself. It's important to submit both the form and any required payment by this date to avoid potential penalties and interest for late submissions.

How do I calculate the taxes owed on the 450 Tennessee Form?

The form requires you to add your gross sales, the cost of personal property purchased but used, out-of-state purchases, and the fair market value of fabricated property. From this total, subtract any exempt transactions. Then, apply the appropriate tax rates provided on the form to calculate your state and local taxes owed, as well as any applicable special taxes like the Prepaid Wireless 911 Surcharge.

What are exempt transactions on the 450 Tennessee Form?

Exempt transactions can include, but are not limited to, sales made to vendors for resale, purchases by qualified nonprofit institutions, sales paid for with SNAP benefits, and sales during the Sales Tax Holiday. The form provides a section, Schedule A, where these exemptions should be detailed.

What should sellers located outside Tennessee know about the 450 Tennessee Form?

For sellers located outside Tennessee but making sales into the state, it's important to report sales based on the delivery destination within Tennessee. Schedule E of the form is specifically designed for these transactions, helping outside sellers accurately report their sales and apply the correct local tax rates.

Common mistakes

When filling out the 450 Tennessee Sales and Use Tax Return form, several common mistakes can lead to errors in processing or potential penalties. By recognizing these pitfalls, filers can ensure a smoother submission process.

- Not rounding to the nearest dollar: As instructed, all figures should be rounded to the nearest dollar, yet many overlook this detail, leading to unnecessary errors in calculation.

- Inaccurate gross sales reporting: The first item requires reporting of gross sales accurately. Errors here affect the entire form since many subsequent calculations depend on this initial figure.

- Incorrectly reporting exempt transactions: Often, taxpayers fail to correctly identify or calculate exempt transactions, such as sales made to other vendors for resale or items paid for with SNAP benefits. This can result in inaccurate taxable income reports.

- Failure to account for out-of-state purchases: Out-of-state purchases brought into Tennessee for use are taxable. Many forget to include these amounts, thereby underreporting their tax liability.

- Misunderstanding tax rates: Applying incorrect tax rates, especially differentiating between state sales and use tax versus food tax, leads to miscalculations. Understanding the specific tax rate applicable to each transaction is crucial.

- Overlooking location-based taxation: For sellers located outside Tennessee, it's mandatory to report sales using the tax rate applicable to the delivery destination. Ignoring this requirement can result in not only incorrect tax calculations but also compliance issues.

- Omitting special tax rates and fees: Special items such as the Central Business Improvement District Fee or transactions subject to single article tax rates often get missed. It’s important to review all schedules for applicable taxes or fees.

- Improper use of credits: Misapplication of credit memo balances towards the net tax due can complicate the tax return. Understanding when and how to apply credits appropriately is key to accurate filings.

- Including sales tax collected in excess: Line 11 requires reporting of tax collected in excess of the state and local levies. This is frequently overlooked or misunderstood, potentially leading to incorrect total tax due calculations.

- Neglecting to sign the return: An unsigned tax return is considered incomplete and will not be processed. It's a simple but surprisingly common mistake to leave the taxpayer and preparer signature sections blank.

By addressing these common errors, taxpayers can enhance the accuracy of their submitted 450 Tennessee Sales and Use Tax Return. Paying close attention to detail, thoroughly reviewing the instructions, and double-checking calculations prior to submission are essential steps to avoid these pitfalls.

Documents used along the form

When dealing with the complexities of sales and use taxes in Tennessee, the RV-R0012001 form, better known as the Tennessee Department 450 Sales and Use Tax Return, is a critical document for businesses. This form helps businesses in Tennessee report and pay their state and local sales and use taxes. However, to ensure full compliance and accuracy in your tax reporting, there are several other forms and documents that often accompany the Form 450. Below is a rundown of some of these essential documents.

- Schedule A - Exempt Transactions: This is detailed documentation for reporting exempt transactions that should not be included in the taxable total. It requires certificates of resale or other proofs for certain exemptions.

- Schedule B - Local Sales and Use Tax: For reporting local sales and use taxes owed based on county or city jurisdiction. It adjusts the state net taxable total by considering local exemptions and deductions.

- Schedule C - State Single Article Tax and Special Tax Rates: Used for reporting sales of single articles priced between $1,600 and $3,200, and for special tax rate products, detailing state and local taxes due.

- Schedule D - Central Business Improvement District (CBID) Tax: Required for businesses within a designated CBID, this schedule calculates additional fees due based on net sales.

- Schedule E - Destination Sales Report: For businesses located outside Tennessee, this report helps determine the sales tax rate based on the buyer's location.

- Business Tax Application: New businesses must complete this form to register for sales and use tax collection in Tennessee.

- Certificate of Resale: This certificate allows businesses to buy goods tax-free if the goods are intended to be resold.

- Exemption Certificate: Similar to the Certificate of Resale, this document is used to purchase goods without paying sales tax when the goods qualify for a legal exemption.

Together, these documents play a vital role in the accurate reporting and paying of sales and use taxes in Tennessee. Each form addresses specific circumstances and transactions, ensuring businesses meet their tax obligations fully and accurately. By understanding and using these forms in conjunction with the Form 450, businesses can streamline their tax processes, ensure compliance, and avoid potential penalties.

Similar forms

The 450 Tennessee form, designed for state and local sales and use tax returns, shares commonalities with several other tax-related documents, each tailored to specific fiscal responsibilities and reporting requirements. One such document is the Form 1040 used for federal individual income tax returns. Like the 450 Tennessee form, the Form 1040 collects detailed income information, calculates owed taxes, and identifies any applicable deductions or credits, ensuring individuals comply with federal tax obligations.

Another comparable document is the Uniform Sales & Use Tax Exemption/Resale Certificate, Multi-Jurisdiction. This certificate allows businesses to purchase goods tax-free that will be resold, similar to the resale exemption sections on the 450 Tennessee form. Both forms require businesses to declare their intention to resell purchased goods, preventing double taxation by exempting these transactions from sales tax.

The Schedule C (Form 1040) document, used by sole proprietors to report profits or losses from a business, also parallels the 450 Tennessee form’s function. It deals with business income, similar to how the Tennessee form deals with business sales, allowing for the detailing of income, expenses, and applicable deductions to accurately report business performance.

Comparable in its domain is the Form W-2, which employers use to report employee income and withholdings to the federal government. Although it focuses on payroll, the W-2 shares the 450 Tennessee form's objective of reporting financial transactions to taxation authorities, ensuring accurate taxation based on reported figures.

The Value Added Tax (VAT) Return is another analogous document but for international use, particularly in countries that use VAT instead of sales tax. Much like the 450 Tennessee form, it details taxable sales and purchases, allowing businesses to report the amount of VAT they have collected and are accountable to remit to the government.

State Unemployment Tax Act (SUTA) reporting forms, while focusing on unemployment contributions rather than sales tax, mirror the Tennessee document in structure. They require employers to report wages paid to workers, calculate taxes due, and submit this financial information to state authorities.

Excise Tax Forms, used for reporting taxes on specific goods like alcohol, tobacco, and fuel, share the Tennessee form’s specific focus on sales and use but within specialized sectors. Both document types require the reporting of sales amounts and the calculation of taxes due based on those sales.

Lastly, the Business Personal Property Tax Forms, required by various localities, necessitate businesses to list the value of all non-real estate assets. Similar to the 450 Tennessee form, these forms help local governments assess the tax based on the reported value of business property, aiming to tax the use or ownership of such properties.

Each of these documents, while serving unique tax reporting needs, collectively underscores the broad spectrum of taxation from individual income to specific business transactions. The 450 Tennessee form encapsulates a vital fragment of this spectrum, focusing on sales and use tax within the state, reflecting the diverse nature of tax obligations businesses and individuals must navigate.

Dos and Don'ts

Filling out the 450 Tennessee Form, a state and local sales and use tax return, is a crucial process for businesses to ensure compliance with Tennessee’s tax laws. To assist in this task, here are four essential dos and don'ts:

Do:- Ensure accuracy when reporting gross sales and purchases. Take the time to carefully calculate and enter the total amount from lines 1 through 4. This is the foundation of your tax liability and must be correct.

- Thoroughly document exempt transactions. Proper documentation is vital for exempt transactions listed on Schedule A. This clarity will help in case of an audit.

- Include all relevant deductions and fees. Besides basic sales, make sure to account for specific fees and deductions, such as the Central Business Improvement District Fee and the Prepaid Wireless 911 Surcharge, to ensure the accurate calculation of net tax due.

- Double-check for accuracy and completeness. Before submitting, verify that all information is correct and that no required fields have been missed. This includes checking the math on calculated taxes and ensuring that any credits or exemptions are duly noted and supported by documentation.

- Round figures inappropriately. When entering figures, round to the nearest dollar as instructed but do not round prematurely in intermediate calculations to ensure accuracy.

- Forget to report out-of-state and online sales. If your business is located outside Tennessee or sells products online to Tennessee residents, use Schedule E to report these sales correctly based on the destination of the sale.

- Overlook special tax rates and fees. Schedules C and D include elements for single article tax rates and special district fees. Ensure these are not overlooked as they can significantly affect the tax due.

- Delay submission beyond the due date. Submitting the form late can result in penalties and interest charges. Always strive to submit the form and the payment by the due date indicated on the form.

Adhering to these guidelines when completing the 450 Tennessee Form will help ensure that your submission is accurate, complete, and compliant with state tax regulations.

Misconceptions

There are several common misconceptions about the Tennessee Form SLS 450, which is used to report state and local sales and use tax. Understanding these misconceptions can help taxpayers accurately fulfill their reporting and payment obligations.

Misconception 1: Personal property purchased for resale but later used by the business does not need to be reported.

This is incorrect. Personal property purchased on a resale certificate but then used by the business must be declared (on Line 2 of the form). Taxpayers are required to pay sales tax on the cost of these items.

Misconception 2: All out-of-state purchases are exempt from Tennessee sales tax.

Actually, out-of-state purchases brought into Tennessee for use (reported on Line 3) are subject to sales tax unless specifically exempt. This ensures fairness between in-state and out-of-state vendors.

Misconception 3: Sales tax rates are uniform across Tennessee.

In reality, local sales and use tax rates vary by jurisdiction. The SLS 450 form requires taxpayers to calculate local taxes (Line 10) based on the specific rates applicable to their business location(s), as well as the destination of sales for out-of-state sellers.

Misconception 4: Tax collected in excess of state and local levies need not be reported.

Contrary to this belief, tax collected beyond the required amounts (Line 11) must be reported and remitted. Over-collecting sales tax without remitting it can result in penalties.

Misconception 5: A separate form is needed for each business location.

This is not the case. Schedule E of the SLS 450 allows sellers, especially those located outside Tennessee, to report sales by location. This schedule ensures that sales are taxed according to the correct local rate, supporting accurate reporting on a single form.

Misconception 6: The Central Business Improvement District (CBID) fee applies only to retail sales.

Actually, the CBID fee (Line 14) may also apply to sales of services, lodging to transients, alcohol subject to the LBD tax, and several other categories of sales, not solely to retail sales.

Understanding and correcting these misconceptions can help ensure compliance with Tennessee's sales and use tax laws, prevent audit issues, and avoid potential penalties and interest for incorrect reporting.

Key takeaways

Filling out and using the 450 Tennessee form, officially known as the State and Local Sales and Use Tax Return, is a crucial process for businesses operating within Tennessee. Here are six key takeaways to ensure accurate and compliant submissions:

- Timely Submission: It's essential to pay close attention to the due date specified on the form to avoid penalties and interest. The Tennessee Department of Revenue encourages taxpayers to submit their return and payment electronically through their website, as this can streamline the process and help prevent delays.

- Accurate Documentation of Sales: Gross sales, including the cost of personal property purchased on a resale certificate but used by the business, out-of-state purchases, and property imported into Tennessee for use, must be accurately reported. This comprehensive documentation forms the basis for calculating the total sales and purchases.

- Understanding Exemptions: Schedule A of the form allows businesses to report exempt transactions. These can include sales made to vendors for resale, sales of items paid for with SNAP benefits, and sales to federal or Tennessee governments and qualified nonprofit institutions, among others. Proper documentation of these exemptions is crucial for accurate tax calculation.

- Calculating Net Tax Due: The form requires businesses to calculate the net tax due by adding state and local sales and use tax, including special tax rates for certain transactions. Businesses must be diligent in applying the correct tax rates, including the provision for prepaid wireless 911 surcharges.

- Accounting for Special Circumstances: The form includes sections for reporting sales subject to special tax rates, such as the state single article tax for sales of single items priced between $1,600 and $3,200, and taxes on specific products or services like industrial water and aviation fuel. It's important to review these sections carefully to ensure all relevant sales are reported accurately.

- Penalties and Interest: If a return is filed late or payment is delayed, businesses must calculate the penalty and interest due and add these amounts to the total tax due. Understanding how to accurately compute penalties can help businesses estimate their total liability in cases of delayed filing or payment.

By meticulously following the instructions provided and ensuring all applicable sales, exemptions, and special circumstances are accurately reported, businesses can fulfill their tax obligations efficiently and effectively, maintaining compliance with Tennessee's sales and use tax requirements.

Popular PDF Forms

Qualified Income Trust Tennessee - Setting up a QIT requires creating a trust document, signed by both the grantor and trustee, and notarized.

Tn Sales Tax Exemption Form - Establishes a clear channel for communication and assistance regarding the use of the tax exemption certificate.

Tennessee Business - Designating a registered agent on the SS-4482 is a legal requirement for ensuring reliable contact between the state and the LLP.