Fill Out a Valid Tennessee Bus 415 Form

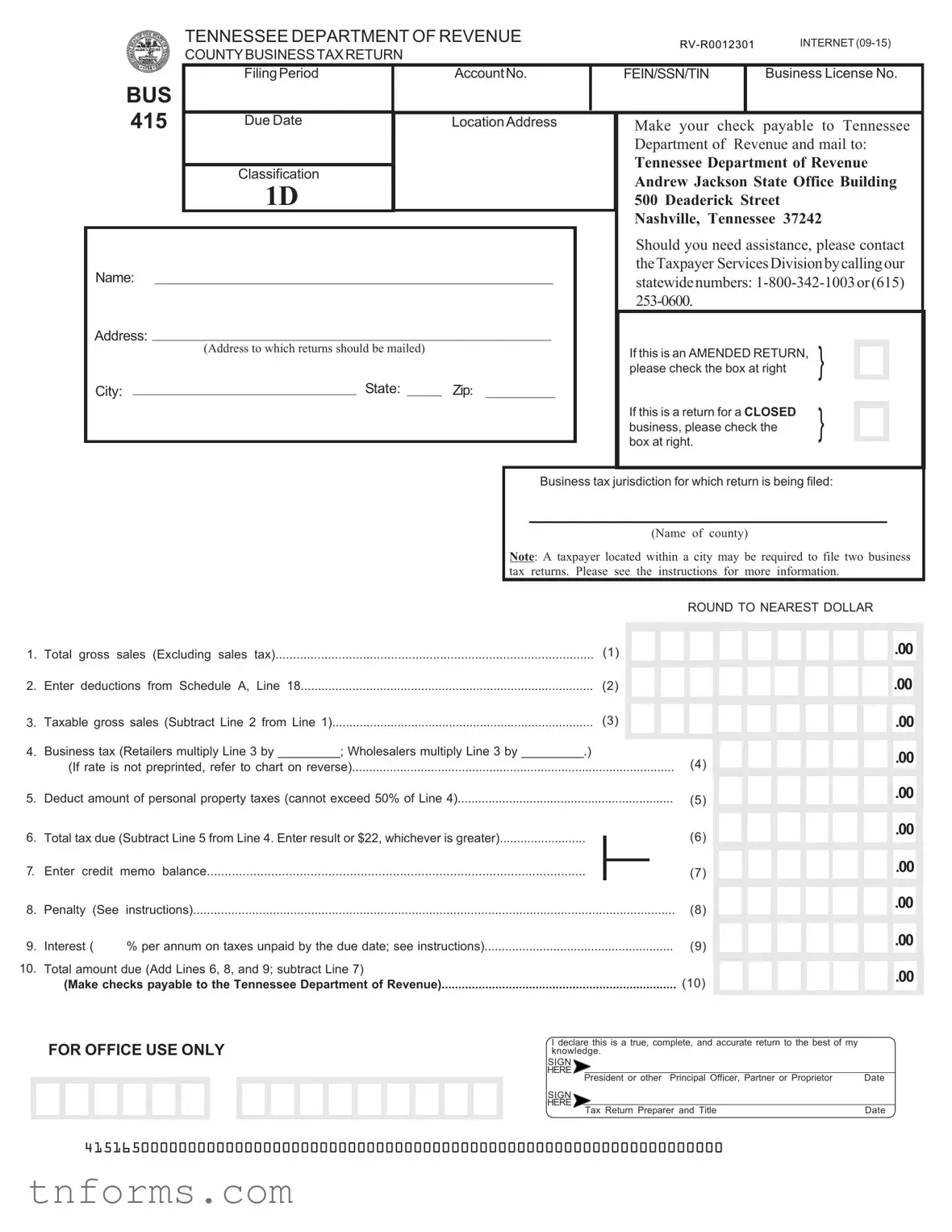

In Tennessee, businesses are required to manage their financial and tax obligations with great care, and the Tennessee Bus 415 form plays a critical role in this process. This form, officially known as the "County Business Tax Return," is a comprehensive document designed for business owners to report their annual earnings and calculate the taxes owed to the state. It covers several important sections, including the reporting of total gross sales (excluding sales tax), deductions permissible under the law, the calculation of taxable sales, and, ultimately, the business tax due. Additionally, the form provides space for adjustments such as credits, penalties, and interest on unpaid taxes by the due date. The flexibility of the form allows for adjustments based on whether it is an amended return or for a business that has closed down. Businesses engaged in both retail and wholesale have different tax rates applied, which are clearly specified in the form, alongside the due dates to ensure timely compliance. For businesses that might need assistance, contact information for the Tennessee Department of Revenue is readily available. The Bus 415 form also includes an appendix for deductions, ranging from sales of services to out-of-state customers to federal and Tennessee-specific taxes that have been paid, ensuring that businesses can accurately account for all eligible reductions in taxable income. Understanding and accurately completing the Bus 415 form is essential for businesses to meet their tax obligations and avoid potential penalties related to late or inaccurate filings.

Example - Tennessee Bus 415 Form

TENNESSEE DEPARTMENT OF REVENUE

COUNTYBUSINESSTAXRETURN

|

|

FilingPeriod |

|

AccountNo. |

|

|

FEIN/SSN/TIN |

|

Business License No. |

|

|||||||||||||||||||

|

BUS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

415 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Due Date |

|

LocationAddress |

|

|

|

|

Make your |

check payable |

to Tennessee |

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

Department of Revenue and mail to: |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

Tennessee Department of Revenue |

|

|||||||||||||||||

|

|

Classification |

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

Andrew Jackson State Office Building |

|

||||||||||||||||||

|

|

1D |

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

500 Deaderick Street |

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

Nashville, Tennessee 37242 |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

Should you need assistance, please contact |

|

|||||||||||||||||

|

Name: _________________________________________________________ |

|

|

|

|

theTaxpayer ServicesDivisionbycallingour |

|

||||||||||||||||||||||

|

|

|

|

|

statewidenumbers: |

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Address: _________________________________________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

(Address to which returns should be mailed) |

|

|

|

|

|

|

If this is an AMENDED RETURN, |

} |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

please check the box at right |

|

|

|

|

|

|

|

||||||||||||

|

City: ________________________________ State: _____ |

Zip: __________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

If this is a return for a CLOSED |

} |

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

business, please check the |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

box at right. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business tax jurisdiction for which return is being filed: |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

(Name of county) |

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

Note: A taxpayer located within a city may be required to file two business |

|

|||||||||||||||||||||||

|

|

|

|

|

tax returns. Please see the instructions |

for more information. |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ROUND TO NEAREST DOLLAR |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. Total gross sales (Excluding sales tax) |

|

|

(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. Enter deductions from Schedule A, Line 18 |

|

|

(2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

||||||

|

............................................................................ |

|

|

|

|

(3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3. Taxable gross sales (Subtract Line 2 from Line 1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Business tax (Retailers multiply Line 3 by _________; Wholesalers multiply Line 3 by _________.) |

|

|

|

|

|

(If rate is not preprinted, refer to chart on reverse) |

(4) |

|||

5. |

Deduct amount of personal property taxes (cannot exceed 50% of Line 4) |

(5) |

|||

6. |

Total tax due (Subtract Line 5 from Line 4. Enter result or $22, whichever is greater) |

|

(6) |

||

|

|||||

7. |

Enter credit |

memo balance |

|

|

|

|

(7) |

||||

8. |

Penalty (See |

instructions) |

|||

9. |

Interest ( |

% per annum on taxes unpaid by the due date; see instructions) |

(9) |

||

10. |

Total amount due (Add Lines 6, 8, and 9; subtract Line 7) |

|

|

|

|

|

(Make checks payable to the Tennessee Department of Revenue) |

(10) |

|||

.00

.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

FOR OFFICE USE ONLY

I declare this is a true, complete, and accurate return to the best of my knowledge.

SIGN

HERE

|

President or other Principal Officer, Partner or Proprietor |

Date |

|

SIGN |

|

||

HERE |

|

|

|

Tax Return Preparer and Title |

Date |

||

|

|||

41516500000000000000000000000000000000000000000000000000000000000000

INTERNET

Schedule A. Deductions from Gross Sales |

|

1. Sales of services received by persons located in other states |

(1) |

2. Returned merchandise when the sales price is refunded to the customer |

(2) |

.00

.00

.00

.00

3.Sales in interstate commerce where the purchaser takes possession outside Tennessee for use or consumption outside Tennessee.......................................................................................................

4.Cash discounts allowed and taken on sales.......................................................................................

5.Repossessions - The portion of the unpaid principal balance in excess of $500 due on tangible per- sonal property repossessed from customers.......................................................................................

6.The amount allowed as

7.Bad debts written off during the reporting period and eligible to be deducted for federal income tax purposes.........................................................................................................................................

8.Amounts paid by a contractor to a subcontractor holding either a business license or contractor's license for performing activities described in Tenn. Code Ann. Section

complete Schedule B and file with the return......................................................................................

Federal and Tennessee privilege and excise taxes:

(3)

.00

.00

(4)

.00

.00

(5)

.00

.00

(6)

.00

.00

(7)

.00

.00

(8)

.00

.00

(Note: All deductions must have adequate records maintained to substantiate deductions claimed or they will be disallowed.)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

...............................................................................................9. Federal and Tennessee gasoline tax |

(9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

10. |

Federal and Tennessee motor fuel tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

(10) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

||

11. |

Federal and Tennessee tobacco tax on cigarettes |

(11) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

12. Federal and Tennessee tobacco tax on all other tobacco products |

(12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13.Federal and Tennessee beer tax....................................................................................................

14.Tennessee special tax on petroleum products........................................................

15.Tennessee liquified gas tax for certain motor vehicles..............................................

16.Tennessee beer wholesale tax..........................................................................................................

17.Other deductions not taken elsewhere on the return.........................................................................

(Specify)

18. Total Deductions. Add Lines 1 through 17. Enter here and in Page 1, Line 2 |

(18) |

(13)

.00

.00

(14)

.00

.00

(15)

.00

.00

(16)

.00

.00

(17)

.00

.00

.00

.00

CLASSIFICATION |

RETAILER RATES |

WHOLESALER RATES |

TAX PERIOD |

DUE DATE |

Class 1A |

0.001 |

0.00025 |

|

|

Class 1B & 1C |

0.001 |

0.000375 |

|

Not later than the |

Class 1D |

0.0005 |

Notapplicable |

|

15th day of the 4th |

Class 1E |

Notapplicable |

0.0003125 |

Fiscal Year |

month following the |

Class 2 |

0.0015 |

0.000375 |

|

end of the tax |

Class 3 |

0.001875 |

0.000375 |

|

period. |

Class 4 |

0.001 |

Not applicable |

|

|

Class 5 |

0.003 |

Not applicable |

|

|

|

|

|

|

|

Form Breakdown

| Fact Number | Description |

|---|---|

| 1 | The form is named BUS 415 and is required for filing county business tax returns in Tennessee. |

| 2 | This form is issued by the Tennessee Department of Revenue. |

| 3 | It is used by businesses to report total gross sales, deductions, taxable gross sales, and personal property taxes. |

| 4 | Payments made using this form should be payable to the Tennessee Department of Revenue. |

| 5 | The form requires identification numbers such as FEIN/SSN/TIN and the Business License No. |

| 6 | Tax-related inquiries can be directed to the Taxpayer Services Division using the provided statewide numbers. |

| 7 | The form includes specific sections for amended returns or notification of a closed business. |

| 8 | Governing laws for this form include federal and Tennessee privilege and excise taxes, covering several specific taxes such as gasoline, motor fuel, tobacco, and beer taxes. |

Detailed Instructions for Filling Out Tennessee Bus 415

Filing the Tennessee Department of Revenue County Business Tax Return, known as BUS 415, involves a series of steps carefully designed to ensure accuracy and compliance with state tax regulations. It's essential for businesses operating within Tennessee to complete this form diligently, as it plays a vital role in meeting tax obligations for the period under consideration. Whether you're running a retail or wholesale operation, the specifics of your business activities and the corresponding financial details will dictate how the form should be filled out. The following step-by-step instructions will guide you through the process, making it more manageable.

- Begin by entering your business details, including the Filing Period, Account No., and Business License No., along with your FEIN/SSN/TIN. Include the due date for submission at the designated space.

- Fill in your Location Address where the business operates, and if applicable, check the box indicating if this is an Amended Return or for a Closed business.

- Under the section for business tax jurisdiction, input the name of the county for which the return is being filed, noting that businesses within city limits may need to file two returns.

- In the section for financial details, start with your Total Gross Sales, excluding sales tax, in Line 1.

- Proceed to calculate your deductions according to Schedule A at the back, completing it thoroughly before entering the total from Line 18 into Line 2 on the front page.

- Subtract Line 2 from Line 1 to determine your Taxable Gross Sales and enter this on Line 3.

- Calculate your business tax based on the applicable rate (retailer or wholesaler) and enter this in Line 4. Refer to the rate chart on the reverse side if your rate is not preprinted.

- If applicable, enter the amount of personal property taxes in Line 5, ensuring it does not exceed 50% of Line 4's total.

- Calculate the Total Tax Due by subtracting Line 5 from Line 4 and enter the greater of the result or $22 in Line 6.

- Input any credit memo balance in Line 7.

- Refer to the instructions for calculating late penalties and interests, if applicable, and enter these amounts in Lines 8 and 9.

- Sum up the total amount due by adding Lines 6, 8, and 9, subtracting Line 7's value, and enter this in Line 10.

- Complete the form by signing and dating the bottom; include the title if someone other than the principal officer is preparing the return.

- Finally, review the entire form to ensure all information is accurate and complete, then make a check payable to Tennessee Department of Revenue and mail it to the provided address.

Ensuring accuracy and timeliness in submitting the BUS 415 form is crucial for compliance and to avoid potential penalties. The process may seem detailed but paying close attention to each step simplifies fulfilling your business’s tax obligations in Tennessee. Remember, if at any point you require assistance, taxpayer services are available to guide you through the process and answer any questions you might have.

More About Tennessee Bus 415

What is the Tennessee BUS 415 form?

The Tennessee BUS 415 form is a County Business Tax Return required by the Tennessee Department of Revenue. Business owners use this form to report their total gross sales, deductions, taxable gross sales, and calculate the business tax owed to the state. This form is essential for maintaining compliance with Tennessee’s tax laws for businesses operating within the state.

When is the BUS 415 form due?

The BUS 415 form is due no later than the 15th day of the 4th month following the end of the business's fiscal tax period. It's important to adhere to this deadline to avoid penalties and interest charges for late submission.

Where should the BUS 415 form be mailed?

The completed BUS 415 form should be mailed to the Tennessee Department of Revenue at the address listed on the form: Andrew Jackson State Office Building 1D, 500 Deaderick Street, Nashville, Tennessee 37242. Make sure your check, payable to the Tennessee Department of Revenue, is included with your form.

What should I do if this is an amended return?

If you need to amend a previously filed BUS 415 form, you should check the box indicating that this submission is an amended return. This notifies the Tennessee Department of Revenue that you are updating or correcting information on a return that has already been filed.

What is required if the business is closed?

If you are filing a BUS 415 form for a business that has closed, it's important to check the box indicating the return is for a closed business. This lets the Tennessee Department of Revenue know that this will be the final return filed for that particular business entity.

How do I calculate the total tax due?

To calculate the total tax due on the BUS 415 form, subtract the amount of personal property taxes (not to exceed 50% of Line 4) from the business tax (Line 4). Then, add any penalties and interest due (if applicable) and subtract any credit memo balance. The result is the total amount owed to the Tennessee Department of Revenue.

What are some common deductions from gross sales?

Common deductions from gross sales on the BUS 415 form include:

- Sales of services to out-of-state customers.

- Returned merchandise refunds.

- Sales in interstate commerce where the product is taken possession outside Tennessee.

- Cash discounts, repossessions, and trade-in values.

- Bad debts written off and eligible federal and Tennessee taxes paid.

What happens if I file the form late?

If the BUS 415 form is filed after its due date, penalties and interest may be applied. The interest is calculated at a percentage per annum on taxes unpaid by the due date. It is crucial to file on time to avoid these additional charges.

Who should sign the BUS 415 form?

The BUS 415 form must be signed by the President, another principal officer, partner, or proprietor of the business. If a tax return preparer completes the form, they should also sign and indicate their title. This ensures accountability and the accuracy of the information provided.

Can I receive assistance with the BUS 415 form?

Yes, for assistance with the BUS 415 form, you can contact the Taxpayer Services Division by calling the statewide numbers provided on the form: 1-800-342-1003 or (615) 253-0600. They can provide guidance and answer any questions you may have regarding the completion and submission of the form.

Common mistakes

Filling out the Tennessee BUS 415 form, a requirement for reporting business taxes to the Tennessee Department of Revenue, presents several common pitfalls that businesses often encounter. It's crucial to avoid these mistakes to ensure compliance and accuracy in one’s tax obligations.

One common mistake is failing to report the total gross sales accurately on Line 1. Businesses sometimes exclude or mistakenly include sales tax in this figure, which leads to discrepancies in the reported amount. Since this figure is essential for calculating the taxable gross sales, its accuracy is paramount.

Another area where errors often occur is in the deductions section (Schedule A). Businesses either overlook eligible deductions or falsely claim deductions for which they do not maintain adequate records. This oversight not only impacts the accuracy of the reported taxable gross sales but can also lead to audit issues or disallowed deductions due to insufficient documentation.

Incorrectly calculating the business tax on Line 4 by using the wrong tax rate can significantly affect the tax liability. It’s crucial to refer to the chart on the reverse side of the form to apply the correct tax rate for either retailers or wholesalers, depending on the business classification. An incorrect rate can lead to underpaid or overpaid taxes.

Overlooking the option to deduct a portion of personal property taxes on Line 5 is another common oversight. Businesses can deduct up to 50% of their business tax due through personal property taxes paid. Neglecting this opportunity can result in an unnecessary financial burden.

Inaccurately recording the credit memo balance on Line 7 or miscalculating penalties and interest (Lines 8 and 9) can also lead to incorrect total amounts due. These errors can result from misinterpreting the instructions or from simple mathematical errors, but they can substantially affect the total tax liability.

Lastly, businesses often incorrectly address their payment check or fail to sign the form, which may seem minor but can delay processing. The check should be made payable to the Tennessee Department of Revenue, and both the taxpayer and the preparer (if applicable) must sign the form to validate it.

In summary, when completing the Tennessee BUS 415 form, businesses should:

- Ensure total gross sales are reported accurately, excluding sales tax.

- Claim deductions accurately and maintain adequate records for verification.

- Utilize the correct tax rate when calculating the business tax due.

- Take advantage of the personal property tax deduction if applicable.

- Accurately calculate the credit memo balance, penalties, and interest.

- Make the payment check payable to the correct authority and ensure the form is signed.

Avoiding these common mistakes can help streamline the tax reporting process and ensure compliance with Tennessee's tax laws.

Documents used along the form

Filling out the Tennessee BUS 415 form is a necessary step for businesses operating in the state, but it's not the only document they need to handle. Whether starting a new business, managing an existing one, or closing operations, a variety of forms and documents must be navigated. Here's a look at some of the other crucial paperwork often associated with the BUS 415 form.

- Business License Application: Before you can even fill out the BUS 415, you'll likely need to apply for a business license in Tennessee. This form starts the process of legally operating a business in the state.

- Schedule B: Mentioned within the BUS 415 instructions, this document is necessary for contractors to itemize payments made to subcontractors, which can affect deductions on the main tax return.

- Franchise and Excise Tax Returns: Many businesses in Tennessee are also subject to franchise and excise taxes, requiring separate filings that detail the company's financial and operational status.

- Annual Report: Most registered businesses must file an annual report with the Tennessee Secretary of State, providing updated information about the company's activities, leadership, and financial condition.

- Personal Property Tax Schedule: If your business owns tangible personal property, this schedule must be completed and filed to report and pay taxes on these assets.

- Sales and Use Tax Return: Businesses selling goods or certain services in Tennessee must collect sales tax and periodically file this return to remit the tax collected from customers.

- Employer's Tax Guides: If your business has employees, you'll need to comply with federal and state employer tax responsibilities, including withholding, reporting, and paying employment taxes.

- Change of Address Form: Should your business move locations, you'll need to officially update its address with the Tennessee Department of Revenue and other relevant agencies to ensure you receive important tax documents and correspondence.

- Business Tax Closure Form: If closing your business, this form notifies the Department of Revenue to terminate your business tax account and cease tax collection responsibilities.

Understanding and managing the paperwork can seem overwhelming, but keeping on top of these forms ensures that your business complies with Tennessee laws and regulations. Each document plays a critical role in the financial and legal aspects of your business, helping to avoid penalties and keep operations running smoothly. Whether you're completing the BUS 415 form or any related documents, careful attention to detail and deadlines is crucial.

Similar forms

The IRS Form 1040, U.S. Individual Income Tax Return, is quite similar to the Tennessee BUS 415 form in that both forms are used to report income and calculate taxes owed to the government. Just like the BUS 415 form requires business owners to report gross sales, deductions, and the total tax due, the Form 1040 requires individuals to report their income, deductions, and the tax they owe or the refund they are entitled to receive. Both forms also require the taxpayer's identification number, which can be a Social Security Number for individuals or a Federal Employer Identification Number for businesses.

Another document that aligns with the Tennessee BUS 415 form is the IRS Form 1120, which is the U.S. Corporation Income Tax Return. This form is used by corporations to report their incomes, gains, losses, deductions, and to calculate their federal income tax liability. Similar to the BUS 415, Form 1120 includes sections for reporting total income and allowable deductions which determine the net taxable income and subsequent tax owed to the IRS.

The Schedule C (Form 1040), Profit or Loss from Business, shares similarities with the BUS 415 form as well. Used by sole proprietors to report the income or loss from a business they operated or a profession they practiced, Schedule C includes the reporting of gross receipts, expenses, and the calculation of the net profit or loss from the business. Like the BUS 415 form, it affects a taxpayer’s overall tax liability and requires detailed financial information.

Form 941, Employer's Quarterly Federal Tax Return, although primarily focusing on payroll taxes, bears resemblance to the BUS 415 form in its function of reporting to a government agency. Form 941 is used by employers to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks and also reports the employer's portion of social security or Medicare tax. While BUS 415 focuses on business taxes, both forms serve to calculate and report taxes owed to federal or state authorities.

The State Unemployment Tax Act (SUTA) filings, while specific to unemployment insurance, are analogous to the BUS 415 form because both involve reporting financial information that affects tax liability. Businesses file SUTA reports to state agencies, detailing wages paid to employees to determine the employer’s unemployment tax rate. Like the BUS 415, these filings are essential for compliance with tax obligations and affect the financial operations of a business.

IRS Form 1065, U.S. Return of Partnership Income, parallels the BUS 415 form in its purpose of reporting income, deductions, and taxes owed, but does so for partnerships. This form collects information about a partnership’s financial activities over the year and is used to assess the total tax liability the partnership faces. Both forms require detailed accounting of business activities and directly impact the taxation process.

The IRS Form 990, Return of Organization Exempt from Income Tax, shares a common goal with the BUS 415 form in terms of reporting financial activities, albeit for a different audience. Form 990 is filed by nonprofits to provide the IRS with information on their operations, including revenue and expenses. This form ensures that organizations adhere to the laws governing tax-exempt status, similar to how the BUS 415 ensures businesses comply with state business tax laws.

The U.S. Customs and Border Protection Form 7501, Entry Summary, also shares similarities with the BUS 415 form in its role in calculating taxes payable to the government, but in the context of importing goods into the United States. It requires detailed descriptions of the merchandise, its value, and the applicable duty rate to calculate the amount of duty owed. Just as the BUS 415 entails the reporting of in-state business operations and the resulting tax, Form 7501 focuses on the importation process and its associated taxes.

The Sales and Use Tax Return, which varies by state, is inherently similar to the BUS 415 form as they both deal with the taxation of business transactions. These forms require businesses to report the total sales made within a specific period, the amount of tax collected from customers, and calculate the tax due to the state. Like the BUS 415, the Sales and Use Tax Return plays a crucial role in fulfilling a business's tax obligations.

Lastly, the Annual Report filed with the Secretary of State, required by many states for registered businesses, although not a tax document, contains elements akin to the BUS 415 form. This report often includes information about the business’s operations, management, and location. While its primary purpose is to keep the public record updated, it shares the commonality of reporting business specifics, crucial for regulatory compliance and taxation purposes, similar to what BUS 415 demands for local tax obligations.

Dos and Don'ts

When preparing to fill out the Tennessee Bus 415 form, understanding the guidelines can help ensure the process is completed accurately and efficiently. Below are ten tips divided into what individuals should and shouldn't do during this process.

What You Should Do:- Review the entire form first: Before filling out the form, take a moment to review all sections fully to understand what information is required.

- Gather necessary documents: Collect all relevant documents related to gross sales, deductions, tax calculations, and personal property taxes to have all the information readily available.

- Use accurate and up-to-date information: Ensure all the data entered, from the business license number to gross sales figures, is correct and current to avoid discrepancies.

- Round to the nearest dollar: When entering financial amounts, round your figures to the nearest dollar as instructed on the form to ensure consistency.

- Check for specific classifications and rates: Determine your business classification and applicable tax rate carefully to calculate your taxes accurately.

- Sign the form: Make sure the form is signed by the authorized person, such as the President, Partner, or Proprietor, and the Tax Return Preparer, if applicable.

- Keep a copy for your records: After submitting the form, retain a copy for your business records in case it is needed for reference or verification in the future.

- Don't leave sections blank: Complete every section of the form. If a section does not apply, indicate with a 'N/A' or '0', as appropriate, to show that it was not overlooked.

- Don't estimate figures: Avoid using estimated amounts. Use actual figures from your records for sales, deductions, and taxes to ensure accuracy.

- Don't ignore instructions: Each part of the form may have specific instructions, such as how to calculate deductions or apply for credits. Make sure these are followed exactly to avoid making errors.

- Don't submit without reviewing: Before sending the form to the Tennessee Department of Revenue, review all entries for completeness and accuracy to prevent any potential delays or questions about your return.

By taking the time to follow these dos and don'ts, you can help ensure that your Tennessee Bus 415 form is filled out properly, reducing the chances of errors and the need for amendments.

Misconceptions

When dealing with the Tennessee BUS 415 form, several misunderstandings can arise. This form is a key component in business operations within Tennessee, demanding attention to detail and an accurate understanding of its requirements and implications. To clarify, here are seven common misconceptions about the Tennessee BUS 415 form:

- It's only for big businesses: Many assume the BUS 415 is exclusively for large corporations. However, this form is relevant for businesses of various sizes, including small and medium enterprises, as long as they are engaged in activities that require reporting and payment of business taxes in Tennessee.

- Only retail businesses need to file it: Another common misconception is that the BUS 415 is solely for retail businesses. In reality, both retailers and wholesalers are required to file this form, with specific sections applicable to each category to ensure proper tax calculation and payment.

- Personal property taxes are fully deductible: While the form allows deductions for certain taxes, including a portion of personal property taxes, it's incorrect to believe that these can be deducted in full. The deduction for personal property taxes cannot exceed 50% of the business tax calculated on the form.

- Filing is only necessary if the business is profitable: Some business owners mistakenly think they need to file the BUS 415 only if their business turns a profit. The requirement to file is based on gross sales, not profitability, mandating businesses to file even in years when they operate at a loss.

- Penalties and interest can be ignored if not preprinted: The assumption that penalties and interest are optional or only apply if preprinted on the form is false. The form includes sections for calculating penalties and interest applicable to late payments, which must be accurately completed to avoid further penalties.

- The form covers all business taxes: While BUS 415 is comprehensive, it's a mistake to believe it encompasses all possible business taxes. Businesses may have other tax liabilities at the federal, state, or local level that require separate filings.

- Amended returns are unnecessary: Some believe that once the BUS 415 is filed, any errors or omissions cannot or should not be corrected. Contrary to this belief, the form provides an option for filing an amended return, allowing businesses to correct previous submissions to ensure accurate reporting and compliance.

Understanding the specifics of the Tennessee BUS 415 form is crucial for businesses operating within the state. Misconceptions can lead to mistakes in filing and potentially result in penalties or other legal issues. Businesses should strive for a thorough comprehension of this form's requirements, ensuring compliance with state tax regulations.

Key takeaways

Filling out and correctly using the Tennessee BUS 415 form is essential for ensuring compliance with the Tennessee Department of Revenue's requirements for business taxes. Below are key takeaways to assist in this process:

- Accuracy is crucial: The BUS 415 form requires detailed information about your business's gross sales, deductions, and taxable gross sales. It's important to round numbers to the nearest dollar and ensure all calculations are accurate to avoid errors that could lead to penalties or audits.

- Deductions need to be substantiated: Deductions can significantly impact your taxable amount. However, it's essential to maintain records that substantiate any deductions claimed on Schedule A of the form, as failure to provide adequate documentation upon request can result in those deductions being disallowed.

- Know your classification and applicable rates: The form differentiates between retailers and wholesalers, with different tax rates applied to each category. Identifying your correct classification and applying the appropriate rate is critical in calculating the tax due correctly.

- Penalties and interest: Late filings or payments can incur penalties and interest. The form provides guidance on calculating these additional costs, emphasizing the importance of meeting the deadline to avoid unnecessary expenses.

- Special circumstances: The form allows for reporting special circumstances such as amending a previously filed return or reporting for a closed business. Checking the appropriate box for these situations ensures that the Department of Revenue processes your return according to your current business state.

It is imperative for businesses operating within Tennessee to familiarize themselves with the BUS 415 form's requirements. Proper and timely filing helps maintain compliance with state tax laws, contribute to the smooth operation of your business, and avoid potential penalties. For any questions or need for assistance, reaching out to the Tennessee Department of Revenue's Taxpayer Services Division is advisable.

Popular PDF Forms

Workers Comp Exemption Tn - A crucial form in the Tennessee workers' compensation process, detailing the extent of an employee's work-related injuries.

Tennessee Division of Corporations - Provides a legal avenue for LLCs to adapt to growth, restructuring, or changes in business environment by amending foundational documents.