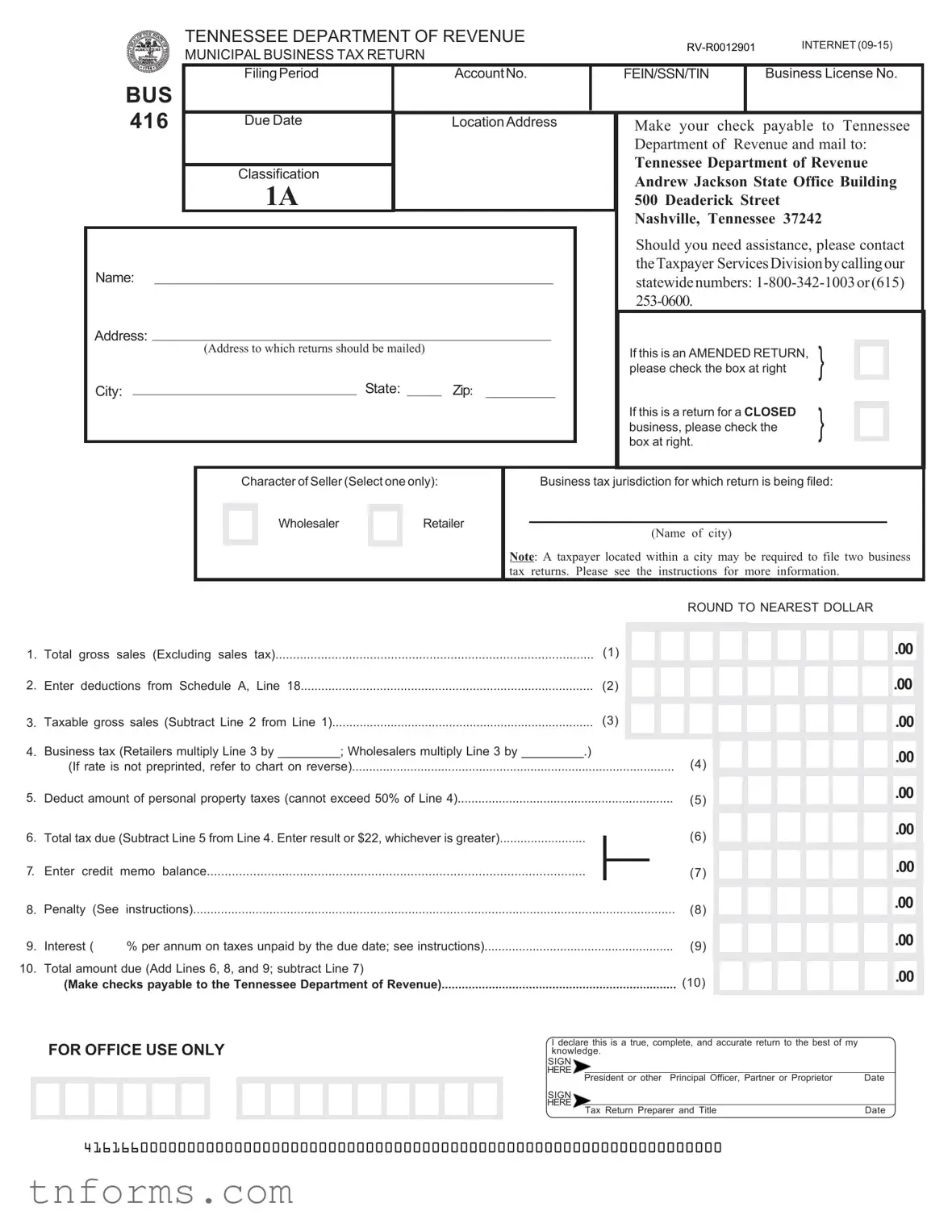

Fill Out a Valid Tennessee Bus 416 Form

Filing taxes can be a daunting task for businesses, but understanding specific forms like the Tennessee Bus 416, the Municipal Business Tax Return, can simplify the process significantly. This form, administered by the Tennessee Department of Revenue, is essential for businesses operating within the state, encompassing various aspects including filing periods, account numbers, and necessary business license numbers. It requires detailed financial information such as total gross sales, deductions, and taxable gross sales, which are crucial for accurate tax calculation. Additionally, the form offers instructions for certain scenarios like amending a return or closing a business. With categories for wholesalers and retailers, it catulates taxes differently based on the business type, also allowing for deductions such as personal property taxes, returned merchandise, and bad debts. Penalties and interest due for late filing are clearly outlined, emphasizing the need for timely submission. This form is not just a tax return; it also serves as a declaration of a business's annual sales activity, underlining its importance in the compliance with state tax laws. Businesses need to pay careful attention to the classification rates and due dates provided, ensuring they meet their fiscal responsibilities to the state. For those seeking assistance, contact details for the Taxpayer Services Division are readily available, making support accessible for all businesses navigating this obligatory fiscal duty.

Example - Tennessee Bus 416 Form

TENNESSEE DEPARTMENT OF REVENUE

MUNICIPAL BUSINESS TAX RETURN

INTERNET |

|

|

FilingPeriod |

|

AccountNo. |

|

FEIN/SSN/TIN |

|

Business License No. |

||||||

BUS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

416 |

|

|

|

|

|

|

|

|

|

|

||||

|

Due Date |

|

LocationAddress |

Make your check |

payable |

to Tennessee |

||||||||

|

|

|

|

|

|

|

Department of Revenue and mail to: |

|||||||

|

|

|

|

|

|

|

Tennessee Department of Revenue |

|||||||

|

|

Classification |

|

|

|

|

||||||||

|

|

|

|

|

|

Andrew Jackson State Office Building |

||||||||

|

|

1A |

|

|

|

|

||||||||

|

|

|

|

|

|

500 Deaderick Street |

|

|

|

|

|

|||

|

|

|

|

|

|

|

Nashville, Tennessee 37242 |

|||||||

|

|

|

|

|

|

|

Should you need assistance, please contact |

|||||||

Name: _________________________________________________________ |

|

|

theTaxpayer ServicesDivisionbycallingour |

|||||||||||

|

|

statewidenumbers: |

||||||||||||

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address: _________________________________________________________ |

|

|

|

|

|

|

|

|

|

|

||||

|

|

(Address to which returns should be mailed) |

|

|

|

If this is an AMENDED RETURN, |

} |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

please check the box at right |

|

|

|

|

|||

City: ________________________________ State: _____ |

Zip: __________ |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

If this is a return for a CLOSED |

} |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

business, please check the |

|

|

|

|

|||

|

|

|

|

|

|

|

box at right. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Character of Seller (Select one only):

Wholesaler Retailer

Business tax jurisdiction for which return is being filed:

(Name of city)

Note: A taxpayer located within a city may be required to file two business tax returns. Please see the instructions for more information.

|

|

|

|

|

|

|

ROUND TO NEAREST DOLLAR |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Total gross sales (Excluding sales tax) |

(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Enter deductions from Schedule A, Line 18 |

(2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

(3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Taxable gross sales (Subtract Line 2 from Line 1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Business tax (Retailers multiply Line 3 by _________; Wholesalers multiply Line 3 by _________.) |

|

|

|

|

|

(If rate is not preprinted, refer to chart on reverse) |

(4) |

|||

5. |

Deduct amount of personal property taxes (cannot exceed 50% of Line 4) |

(5) |

|||

6. |

Total tax due (Subtract Line 5 from Line 4. Enter result or $22, whichever is greater) |

|

(6) |

||

|

|||||

7. |

Enter credit |

memo balance |

|

|

|

|

(7) |

||||

8. |

Penalty (See |

instructions) |

|||

9. |

Interest ( |

% per annum on taxes unpaid by the due date; see instructions) |

(9) |

||

10. |

Total amount due (Add Lines 6, 8, and 9; subtract Line 7) |

|

|

|

|

|

(Make checks payable to the Tennessee Department of Revenue) |

(10) |

|||

.00

.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

FOR OFFICE USE ONLY

I declare this is a true, complete, and accurate return to the best of my knowledge.

SIGN

HERE

|

President or other Principal Officer, Partner or Proprietor |

Date |

|

SIGN |

|

||

HERE |

|

|

|

Tax Return Preparer and Title |

Date |

||

|

|||

41616600000000000000000000000000000000000000000000000000000000000000

INTERNET

Schedule A. Deductions from Gross Sales |

|

1. Sales of services received by persons located in other states |

(1) |

2. Returned merchandise when the sales price is refunded to the customer |

(2) |

.00

.00

.00

.00

3.Sales in interstate commerce where the purchaser takes possession outside Tennessee for use or consumption outside Tennessee.......................................................................................................

4.Cash discounts allowed and taken on sales.......................................................................................

5.Repossessions - The portion of the unpaid principal balance in excess of $500 due on tangible per- sonal property repossessed from customers.......................................................................................

6.The amount allowed as

7.Bad debts written off during the reporting period and eligible to be deducted for federal income tax purposes.........................................................................................................................................

8.Amounts paid by a contractor to a subcontractor holding either a business license or contractor's license for performing activities described in Tenn. Code Ann. Section

complete Schedule B and file with the return......................................................................................

Federal and Tennessee privilege and excise taxes:

(3)

.00

.00

(4)

.00

.00

(5)

.00

.00

(6)

.00

.00

(7)

.00

.00

(8)

.00

.00

(Note: All deductions must have adequate records maintained to substantiate deductions claimed or they will be disallowed.)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

...............................................................................................9. Federal and Tennessee gasoline tax |

(9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

10. |

Federal and Tennessee motor fuel tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

(10) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

||

11. |

Federal and Tennessee tobacco tax on cigarettes |

(11) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

12. Federal and Tennessee tobacco tax on all other tobacco products |

(12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13.Federal and Tennessee beer tax....................................................................................................

14.Tennessee special tax on petroleum products........................................................

15.Tennessee liquified gas tax for certain motor vehicles..............................................

16.Tennessee beer wholesale tax..........................................................................................................

17.Other deductions not taken elsewhere on the return.........................................................................

(Specify)

18. Total Deductions. Add Lines 1 through 17. Enter here and in Page 1, Line 2 |

(18) |

(13)

.00

.00

(14)

.00

.00

(15)

.00

.00

(16)

.00

.00

(17)

.00

.00

.00

.00

CLASSIFICATION |

RETAILER RATES |

WHOLESALER RATES |

TAX PERIOD |

DUE DATE |

Class 1A |

0.001 |

0.00025 |

|

|

Class 1B & 1C |

0.001 |

0.000375 |

|

Not later than the |

Class 1D |

0.0005 |

Notapplicable |

|

15th day of the 4th |

Class 1E |

Notapplicable |

0.0003125 |

Fiscal Year |

month following the |

Class 2 |

0.0015 |

0.000375 |

|

end of the tax |

Class 3 |

0.001875 |

0.000375 |

|

period. |

Class 4 |

0.001 |

Not applicable |

|

|

Class 5 |

0.003 |

Not applicable |

|

|

|

|

|

|

|

Form Breakdown

| Fact Number | Fact Detail |

|---|---|

| 1 | The Tennessee Department of Revenue issues the Municipal Business Tax Return, identified as form RV-R0012901 (BUS 416). |

| 2 | This form is applicable for businesses operating within Tennessee, requiring them to report their gross sales, deductible expenses, and calculate the business tax owed. |

| 3 | Businesses must distinguish their character of operation as either a wholesaler or a retailer when filing this return. |

| 4 | Depending on their location, businesses might need to file two separate business tax returns if they are situated within a city's jurisdiction. |

| 5 | The form distinguishes between various classification rates for retailers and wholesalers, which impacts the calculation of the business tax. |

| 6 | Payment and completed forms are forwarded to the Tennessee Department of Revenue, located at the Andrew Jackson State Office Building in Nashville, Tennessee. |

| 7 | The deadline for filing this return is typically the 15th day of the 4th month following the end of the business's fiscal tax year. |

Detailed Instructions for Filling Out Tennessee Bus 416

Filling out the Tennessee Bus 416 form is a straightforward process essential for municipal business tax compliance. This form keeps local governments informed about your business activities and ensures that taxes are appropriately calculated and collected. Accuracy and attention to detail are crucial when completing this form to prevent potential issues or delays with your tax filings. Following the right steps can simplify the process.

- Start by verifying your filing period and account number, ensuring they match your business records.

- Enter your Federal Employer Identification Number (FEIN), Social Security Number (SSN), or Taxpayer Identification Number (TIN) in the designated space.

- Provide your Business License Number in the corresponding field.

- Check the appropriate box if you are filing an amended return or if this is a return for a closed business.

- Clearly print the business's location address, as this can affect jurisdictional tax rates and obligations.

- Select your character of seller – either wholesaler or retailer – since this determination impacts the applicable tax rates.

- Specify the business tax jurisdiction (city name) where this return is being filed. Remember that businesses located within a city may need to file additional returns.

- Calculate and enter your total gross sales, excluding sales tax, then input any deductions according to Schedule A, Line 18.

- Determine your taxable gross sales by subtracting your deductions from your total gross sales.

- Calculate the business tax due by applying the specified tax rate for retailers or wholesalers provided on the form or the attached instructions.

- If applicable, deduct the amount of personal property taxes, not exceeding 50% of the business tax calculated.

- Enter the total tax due, ensuring it is not less than $22.

- Adjust the total by any credit memo balance, penalty for late filing if applicable, and interest due.

- Review the total amount due, which includes any adjustments for credits, penalties, and interest.

- Sign the form, indicating your declaration that the information provided is accurate, complete, and true. Include the date and title for both the principal officer and the tax return preparer (if applicable).

- Ensure all necessary documents, including Schedule A or B if required, are attached and mail your completed form and payment to the Tennessee Department of Revenue at the designated address.

Once your Bus 416 form is filled out and sent, the Department of Revenue will process your municipal business tax return. Timely and accurate filing is crucial to avoid any penalties. Keeping a copy of the form and any communication from the Tennessee Department of Revenue for your records is also a good practice. Should questions or concerns about your return arise, the provided contact details for the Taxpayer Services Division can be a valuable resource for assistance.

More About Tennessee Bus 416

What is the Tennessee Bus 416 form used for?

The Tennessee Bus 416 form is a Municipal Business Tax Return used by businesses operating in Tennessee. It is designed to report gross sales, calculate business tax due, and document any deductions or credits that a business is eligible to claim. This form is mandatory for businesses to accurately report their earnings and calculate the taxes owed to the Tennessee Department of Revenue for a specific filing period.

Who needs to file the Tennessee Bus 416 form?

Any business that operates within Tennessee and is subject to the state's business tax must file the Tennessee Bus 416 form. This applies to both wholesalers and retailers, each of which has different tax rates as indicated on the form. If your business is located within a city's limits, you might be required to file two business tax returns – one for the city and another for the county, depending on local tax jurisdiction rules.

How are taxes calculated on the Tennessee Bus 416 form?

Taxes on the Tennessee Bus 416 form are calculated based on taxable gross sales. Here is a step-by-step insight into the process:

- Report your total gross sales excluding sales tax.

- Deduct allowable expenses listed in Schedule A from your gross sales to find your taxable gross sales.

- Multiply your taxable gross sales by the relevant tax rate for your classification as a retailer or wholesaler. The applicable rates are provided on the form for different classes.

- If eligible, subtract the amount of personal property taxes from your calculated business tax - this cannot exceed 50% of your business tax.

- The final tax due will be the greater of the calculated amount or $22. This is the amount you will need to remit to the Tennessee Department of Revenue.

Where and when to submit the Tennessee Bus 416 form?

The completed Bus 416 form should be made payable and mailed to the Tennessee Department of Revenue. The precise address is provided on the form itself, directing businesses to the Andrew Jackson State Office Building at 1A 500 Deaderick Street, Nashville, Tennessee 37242. As for the deadline, the form must be submitted no later than the 15th day of the 4th month following the end of the tax period. For any assistance required during the process, businesses can contact the Taxpayer Services Division at the statewide numbers provided.

Common mistakes

Filling out the Tennessee Bus 416 form for Municipal Business Tax Return can be a bit tricky, and some common missteps could potentially complicate or delay the process. Understanding these errors can help ensure the submission process is smooth and error-free.

Firstly, one common mistake is incorrect or incomplete identification information. This includes missing FEIN/SSN/TIN numbers or business license numbers. These details are crucial for properly identifying the business and ensuring the correct processing of the form.

- Another frequent error involves the gross sales section. Businesses sometimes include sales tax in their total gross sales number, which should be excluded. Accurate figures are vital to calculate the taxable gross sales correctly.

- When it comes to deductions, a significant mistake is not completing Schedule A or inaccurately reporting the deductions. It is essential to detail all eligible deductions to accurately determine taxable income.

- Calculating the business tax incorrectly is a common mistake, especially if the business tax rate is not pre-printed on the form. Retailers and wholesalers have different rates, and applying the wrong rate can lead to underpayment or overpayment of taxes.

- Misunderstanding the personal property tax deduction is another common error. This deduction cannot exceed 50% of the business tax calculated, and misunderstanding this limit could lead to incorrectly reported figures.

- Improper accounting for credit memo balances occurs when businesses fail to accurately subtract these amounts from the total tax due. This oversight can lead to inaccuracies in the total amount owed.

- Calculating penalties and interests without referring to the guidelines provided results in incorrect figures being reported. It’s crucial to assess penalties and interest based on the specific criteria outlined in the instructions.

- Inadequate record-keeping for deductions is a critical mistake. Without proper documentation, claimed deductions could be disallowed, affecting the total taxable amount.

- Lastly, not properly indicating if the return is for an amended return or a closed business can lead to the form being processed incorrectly, potentially affecting future tax obligations or filings.

Ensuring accurate and complete information, understanding the classification rates, and adhering to the form's instructions can prevent these common mistakes. Keeping thorough records and possibly consulting with a professional for clarification can help navigate the complexities of the Tennessee Bus 416 form, ensuring compliance and avoiding potential pitfalls.

Documents used along the form

When dealing with the process of filing a Tennessee BUS 416 form, which is a Municipal Business Tax Return, it's often just one piece in a larger puzzle of documentation required for complete compliance with state tax obligations. Businesses might find themselves needing additional forms and documents to support or further specify the information on their BUS 416 form. Let's look at some of these documents.

- Schedule B: This schedule is specifically mentioned in the BUS 416 form instructions and is necessary for businesses that pay contractors or subcontractors for activities described under certain sections of Tennessee Code. It helps detail payments made to these contractors, which can affect deductions on the main form.

- Business License Application: Before even worrying about tax returns, a business must apply for a business license in the state of Tennessee. This is a foundational document that legitimizes the business in the eyes of the state and sets the stage for future tax obligations.

- Annual Report for Tennessee Corporations: Though not directly related to the municipal business tax return, most corporations operating in Tennessee are required to file an annual report with the Secretary of State. This report provides updated information about the business, such as corporate address and officers and, in some cases, can impact tax considerations.

- Personal Property Tax Schedule: Many businesses will also need to report and pay personal property taxes on items like equipment and furniture. This schedule accompanies your tax return to detail taxable personal property, with some of this potentially affecting deductions on the BUS 416 form.

Gathering and completing all relevant documents is crucial for accurately filing your Tennessee BUS 416 form and maintaining good standing regarding your tax obligations. Always ensure you have the most current forms and consult with a tax professional if you're unsure about your specific needs.

Similar forms

The Tennessee Bus 416 form serves a specific function in the reporting and payment of municipal business taxes, a role that several other documents also fulfill within different jurisdictions or for various tax types. Understanding these documents can provide insight into the broader landscape of tax reporting and compliance requirements for businesses.

One similar document is the IRS Form 941, Employer's Quarterly Federal Tax Return. This form is used by employers to report federal withholdings from employees for income tax, Social Security, and Medicare. The similarity lies in the requirement for businesses to periodically report and remit taxes collected from another party, though the specifics of the taxes differ significantly.

The Sales and Use Tax Return forms that businesses must file in most states bear resemblance to the Tennessee BUS 416 in that they involve the calculation of taxes due based on the business's sales. These forms typically require the report of total gross sales, deductions for nontaxable sales, and the calculation of taxes owed on the taxable sales.

Another related document is the Annual Franchise Tax Report required by various states for different types of business entities. Though this tax is based on the value of the company rather than its sales, the process of reporting business information and calculating a tax due parallels the Tennessee BUS 416's purpose.

The Employer's Annual Federal Unemployment (FUTA) Tax Return, IRS Form 940, demonstrates similarities in the annual reconciliation of taxes owed to a governmental authority. This form focuses on unemployment tax obligations, contrasting with the sales-based tax of the BUS 416 but similar in its periodic reporting requirement.

For businesses operating with special permits, such as alcohol licenses, there are specific tax forms related to the sales of these items. For instance, the Alcohol Tax Return in various states requires detailed sales reporting and tax calculation similar to the process on the BUS 416, though for a more specialized market.

Business Personal Property Tax Returns, required in many jurisdictions, entail reporting the value of business-owned physical assets for tax purposes. While this form calculates tax based on asset values rather than sales, it shares with the BUS 416 the fundamental principle of reporting business-related values for tax calculation.

Payment of Excise Taxes on specific products or services is another area with corresponding documentation, like the Federal Excise Tax Return for businesses selling certain goods or services subject to these taxes. Similar to the BUS 416, these forms include detailed reporting requirements and tax calculations based on sales or usage.

The Highway Use Tax Return is a specialized form required for businesses operating heavy vehicles on public highways. It involves reporting usage and calculating taxes owed to the state, akin to the BUS 416 form's purpose of calculating tax based on business activity, albeit in a completely different context.

In essence, while the Tennessee BUS 416 form is specific to municipal business taxes within Tennessee, many parallels can be drawn to various other tax documents required at both state and federal levels. Each serves to collect different types of taxes but operates under the overarching principle of reporting business activities or assets to calculate and remit the correct amount of tax due.

Dos and Don'ts

Filling out the Tennessee Department of Revenue Municipal Business Tax Return (Form BUS 416) accurately is crucial for business owners. Here's a list of do's and don'ts to help ensure the process is completed correctly.

Do's:

- Double-check the Filing Period and Account No. fields to ensure accuracy.

- Make sure the FEIN/SSN/TIN and Business License No. are entered correctly.

- Use the correct Location Address where your business operates.

- If filing an amended return or filing for a closed business, correctly check the appropriate box at the top of the form.

- Select the correct Character of Seller, whether you're a Wholesaler or Retailer.

- Round all amounts to the nearest dollar as instructed on the form.

- Accurately calculate and enter your Total Gross Sales, deductions, and the Taxable Gross Sales.

- Refer to the tax rate chart provided on the form to correctly calculate your Business Tax due.

- Include any applicable credits, penalties, and interest in the Total Amount Due.

- Sign and date the form as either the President, Principal Officer, Partner, Proprietor, or Tax Return Preparer.

Don'ts:

- Don't leave any fields blank that are applicable to your business situation. Incomplete forms may result in processing delays.

- Don't underestimate the importance of checking the correct box for amended or closed business returns.

- Don't guess on amounts. Ensure all figure are accurate and substantiated by your financial records.

- Don't overlook the Schedule A section for Deductions from Gross Sales. This section can reduce your taxable amount.

- Don't neglect to maintain adequate records for all deductions claimed, as these must be substantiated if questioned.

- Don't miscalculate the tax due by using the incorrect tax rate for your business classification.

- Don't forget to reduce your Business Tax by the amount of personal property taxes paid, if applicable, without exceeding 50% of your business tax.

- Don't send your payment without making it payable to the Tennessee Department of Revenue, as directed on the form.

- Don't disregard the instructions for penalties and interest if your payment is late.

- Don't send the form to the wrong address. Use the provided address for the Tennessee Department of Revenue.

By following these guidelines, you can help ensure your Municipal Business Tax Return is filed correctly and efficiently, minimizing the risk of errors and potential penalties.

Misconceptions

When dealing with the Tennessee Bus 416 form, a Municipal Business Tax Return, many business owners confront common misconceptions that can lead to confusion or errors in filing. Understanding these misconceptions is crucial to ensure accurate and timely submissions.

- Misconception 1: The form is only for retailers.

In reality, both wholesalers and retailers are required to complete the form, as it includes different sections and tax rates applicable to each type of business. - Misconception 2: All businesses must file the form annually.

The truth is that the filing frequency can vary based on the classification of the business, which may require filing more frequently than just once a year. - Misconception 3: Sales tax is included in the total gross sales figure.

Gross sales should be reported excluding sales tax to accurately reflect the business's taxable revenue. - Misconception 4: Deductions are limited to returns and allowances.

Several deductions are permissible, including sales to out-of-state customers, sales in interstate commerce, and even certain taxes paid. It’s essential to review all allowable deductions that can reduce taxable gross sales. - Misconception 5: The due date is the same for all businesses.

Due dates are determined based on the business's fiscal year and classification, meaning they can differ significantly from one business to another. - Misconception 6: Only physical checks are accepted for payment.

While checks are a common form of payment, there are multiple payment methods available, including electronic payments, which can be faster and more secure. - Misconception 7: Penalties and interest are flat rates.

Penalties and interest are calculated based on the amount of tax due and the length of the payment delay, which means they can vary widely. - Misconception 8: Businesses located within a city do not need to file separate returns for state taxes.

Some businesses may be required to file two business tax returns if they are located within certain jurisdictions to cover both city and state tax liabilities.

Addressing these misconceptions head-on can demystify the process of filing the Tennessee Bus 416 form, leading to more accurate and timely tax submissions. Businesses are encouraged to review the form’s instructions carefully or seek advice from tax professionals to ensure compliance and avoid unnecessary errors.

Key takeaways

Understanding how to correctly fill out and use the Tennessee Bus 416 form is crucial for businesses operating within the state. This guide highlights key takeaways to assist businesses in accurately completing the form and staying compliant with Tennessee tax requirements.

- Identify the Business Classification: It's imperative that you accurately identify whether your business operates as a wholesaler or retailer. This classification affects the tax rate applied to your taxable gross sales and hence, impacts the total tax due.

- Accurately Report Gross Sales and Deductions: Begin by reporting your total gross sales excluding sales tax. Then, carefully itemize and subtract allowable deductions as outlined in Schedule A to arrive at your taxable gross sales. Incorrect reporting can lead to discrepancies and potential audits.

- Calculate Tax, Penalties, and Interest Appropriately: Use the correct tax rate for your classification to calculate the business tax due. If your return is late, be sure to accurately calculate and include penalties and interest to avoid further penalties.

- Understand Deduction Criteria: Deductions can significantly reduce your taxable amount. However, each deduction, from sales of services to out-of-state customers to bad debts written off, must be properly documented and meet specific criteria outlined in Schedule A. Inadequate recordkeeping can lead to disallowed deductions.

- Compliance with Deadlines and Payment Instructions: The due date for the Bus 416 form is the 15th day of the 4th month following the end of your tax period. Payments should be made to the Tennessee Department of Revenue, and it's critical to ensure the check or payment method is properly addressed and includes your account information to avoid processing delays.

By focusing on these key areas, businesses can better navigate the complexities of tax reporting and compliance in Tennessee. Accurate completion and timely submission of the Bus 416 form not only fulfill legal obligations but also minimize the risk of penalties and interest for late or incorrect filings.

Popular PDF Forms

How Do I Get a Quitclaim Deed - Effective tool for changing a property's title among known parties.

How Long Can You Get Unemployment in Tennessee - Acts as a bridge between individual documentation needs and Tennessee's statutory requirements.