Fill Out a Valid Tennessee In 1324 Form

At the heart of professional accountability and ethical practice in Tennessee's accountancy landscape lies the Tennessee In 1324 form, a document that represents an accountant's deliberate transition from active to inactive status. Crafted by the State of Tennessee Department of Commerce and Insurance, specifically under the wing of the Tennessee State Board of Accountancy, this form serves as a crucial affidavit for certified public accountants (CPAs) and licensed public accountants (PAs) who decide to step away from actively offering accountancy services. Through this formally notarized declaration, accountants convey their intent to the Board, affirming that they have ceased to provide or offer to provide the public with any services leveraging their auditing, accounting, management advisory, financial advisory, consulting skills, or tax-related expertise. Moreover, it imposes a clear understanding that the title of CPA or PA can no longer be used without clearly stating 'Inactive.' Compliance with this process ensures adherence to the regulatory framework, mandating ongoing certificate renewals and imposing specific requirements for those who wish to reactivate their license, including the completion of eighty hours of continuing professional education (CPE). Beyond the individual's commitment to professional integrity, this form reflects the broader regulatory mechanisms in place to safeguard the quality and reliability of accountancy services in Tennessee, delineating clear paths for transitions within the profession while meticulously detailing the consequences of non-compliance, thus underscoring the significance of such administrative procedures in maintaining the profession's high standards.

Example - Tennessee In 1324 Form

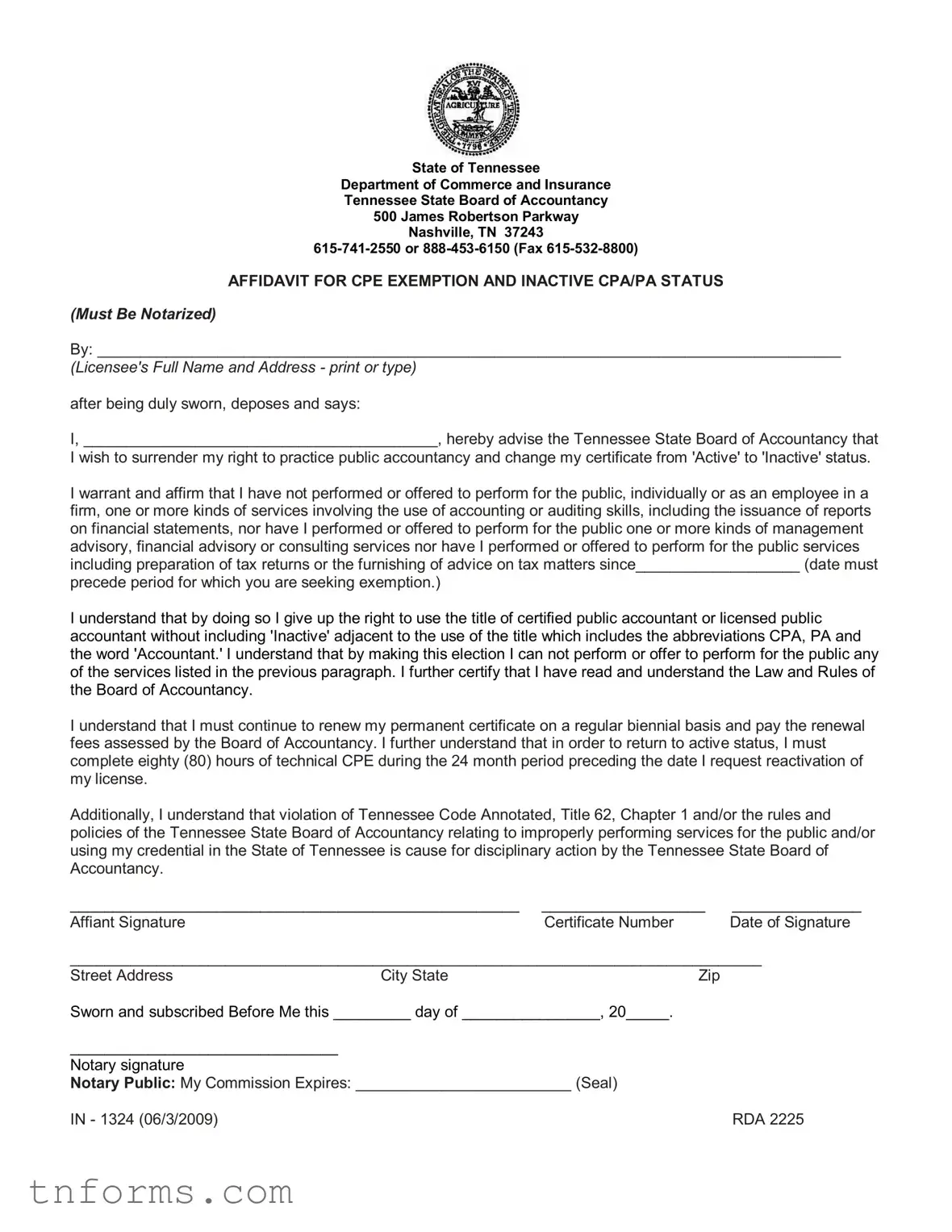

State of Tennessee

Department of Commerce and Insurance Tennessee State Board of Accountancy 500 James Robertson Parkway Nashville, TN 37243

6157412550 or 8884536150 (Fax 6155328800)

AFFIDAVIT FOR CPE EXEMPTION AND INACTIVE CPA/PA STATUS

(Must Be Notarized)

By: ______________________________________________________________________________________

(Licensee's Full Name and Address print or type)

after being duly sworn, deposes and says:

I, _________________________________________, hereby advise the Tennessee State Board of Accountancy that

I wish to surrender my right to practice public accountancy and change my certificate from 'Active' to 'Inactive' status.

I warrant and affirm that I have not performed or offered to perform for the public, individually or as an employee in a firm, one or more kinds of services involving the use of accounting or auditing skills, including the issuance of reports on financial statements, nor have I performed or offered to perform for the public one or more kinds of management advisory, financial advisory or consulting services nor have I performed or offered to perform for the public services including preparation of tax returns or the furnishing of advice on tax matters since___________________ (date must

precede period for which you are seeking exemption.)

I understand that by doing so I give up the right to use the title of certified public accountant or licensed public accountant without including 'Inactive' adjacent to the use of the title which includes the abbreviations CPA, PA and the word 'Accountant.' I understand that by making this election I can not perform or offer to perform for the public any of the services listed in the previous paragraph. I further certify that I have read and understand the Law and Rules of the Board of Accountancy.

I understand that I must continue to renew my permanent certificate on a regular biennial basis and pay the renewal fees assessed by the Board of Accountancy. I further understand that in order to return to active status, I must complete eighty (80) hours of technical CPE during the 24 month period preceding the date I request reactivation of my license.

Additionally, I understand that violation of Tennessee Code Annotated, Title 62, Chapter 1 and/or the rules and policies of the Tennessee State Board of Accountancy relating to improperly performing services for the public and/or using my credential in the State of Tennessee is cause for disciplinary action by the Tennessee State Board of Accountancy.

____________________________________________________ |

___________________ |

_______________ |

|

Affiant Signature |

|

Certificate Number |

Date of Signature |

________________________________________________________________________________ |

|||

Street Address |

City State |

Zip |

|

Sworn and subscribed Before Me this _________ day of ________________, 20_____. |

|

||

_______________________________ |

|

|

|

Notary signature |

|

|

|

Notary Public: My Commission Expires: _________________________ (Seal) |

|

||

IN 1324 (06/3/2009) |

|

|

RDA 2225 |

Form Breakdown

| # | Fact |

|---|---|

| 1 | The form is officially titled "AFFIDAVIT FOR CPE EXEMPTION AND INACTIVE CPA/PA STATUS" and is necessary for CPAs in Tennessee wishing to change their status from 'Active' to 'Inactive'. |

| 2 | It is governed by the Tennessee Code Annotated, Title 62, Chapter 1, and the rules and policies of the Tennessee State Board of Accountancy. |

| 3 | The form must be notarized to affirm the accuracy and truthfulness of the information provided by the applicant. |

| 4 | Applicants declare on this form that they have not performed services involving the use of accounting or auditing skills, management advisory, financial advisory, consulting services, preparation of tax returns, or furnished advice on tax matters since a specified date. |

| 5 | By submitting the form, the licensee agrees to give up the right to practice public accountancy in Tennessee and to use the title "certified public accountant" or "licensed public accountant" without stating 'Inactive' next to it. |

| 6 | The affidavit requires the licensee's full name, address, license number, and signature, along with the date of the signature. |

| 7 | Licensees must continue to renew their certificate biennially and pay the associated fees to maintain their 'Inactive' status. |

| 8 | To return to an 'Active' status, a licensee must complete eighty (80) hours of technical Continuing Professional Education (CPE) within the 24 months prior to their reactivation request. |

| 9 | Violation of the relevant Tennessee laws, rules, or policies is a cause for disciplinary action by the Tennessee State Board of Accountancy. |

| 10 | The form is issued by the Tennessee Department of Commerce and Insurance, specifically under the Tennessee State Board of Accountancy, located at 500 James Robertson Parkway, Nashville, TN. |

Detailed Instructions for Filling Out Tennessee In 1324

Filling out the Tennessee In 1324 form is a crucial step for certified public accountants and licensed public accountants in Tennessee seeking an exemption from continuing professional education (CPE) requirements and wishing to change their status to inactive. This process involves providing personal and license information, affirming that no accountancy services have been offered to the public since a specified date, and understanding the obligations tied to this status change. It's essential to follow each step carefully to ensure the form is completed correctly.

- Start by entering your full name and address in the space provided at the top of the form, ensuring that the information is legible and accurate.

- Next, in the space following "I, _______________," insert your name to affirm that you are officially making the request to the Tennessee State Board of Accountancy.

- In the statement that follows, specify the date since when you have not performed or offered any public accounting services. This date must be before the period for which you're seeking the exemption.

- Review the list of obligations and restrictions associated with changing your certificate status to 'Inactive,' understanding that doing so limits your ability to use certain titles and perform specific services.

- Acknowledge your understanding of the requirements for reactivation of your license by filling in any required information or checking the corresponding boxes, if applicable.

- Sign your name under the "Affiant Signature" line, and enter your certificate number and the date next to your signature.

- Provide your street address, city, state, and ZIP code in the designated areas below your signature.

- Have the affidavit notarized by bringing it to a notary public, who will witness your signature. Complete this step by having the notary fill in the date, sign their name, and provide their commission expiration date along with the notary seal.

Once you have completed all the steps and ensured the information is accurate, submit the form to the Tennessee State Board of Accountancy at the address provided on the form. Remember, switching to an inactive status and applying for a CPE exemption is a significant decision that impacts your professional practice. Make sure to consider all the implications and maintain awareness of the requirements to return to active status, should you choose to do so in the future.

More About Tennessee In 1324

What is the Tennessee IN 1324 form?

The Tennessee IN 1324 form, also known as the Affidavit for CPE Exemption and Inactive CPA/PA Status, is a document used by certified public accountants (CPAs) or licensed public accountants (PAs) in the state of Tennessee to request a change from 'Active' to 'Inactive' status with the Tennessee State Board of Accountancy. By completing this affidavit, the licensee notifies the board that they wish to surrender their right to practice public accountancy and will not offer services involving accounting or auditing skills, management advisory, consulting services, or tax-related services to the public.

Who needs to fill out the IN 1324 form?

CPAs or PAs in Tennessee who want to change their professional status from 'Active' to 'Inactive' must fill out the IN 1324 form. This decision is typically made by accountants who no longer wish to offer public accounting services or meet the continuing professional education (CPE) requirements associated with maintaining an active license.

What are the conditions for applying for Inactive status in Tennessee?

Applicants must meet the following conditions to apply for Inactive status:

- The licensee must not have performed or offered public accounting services since a date preceding the exemption request.

- The licensee agrees not to perform or offer to perform any accounting, auditing, advisory, or tax services as described in the form to the public.

- The licensee must understand that changing to an Inactive status means they cannot use the CPA or PA title without the adjunct 'Inactive'.

- The licensee agrees to continue renewing their permanent certificate biennially and pay the necessary renewal fees.

Does changing to Inactive status affect the use of CPA or PA title?

Yes, changing to Inactive status affects the use of the CPA or PA title. Licensees can no longer use the certified public accountant or licensed public accountant title without adding 'Inactive' adjacent to their title. This includes any abbreviations such as CPA or PA, and even when using the term 'Accountant' in a professional context.

What are the requirements to reactivate a license from Inactive to Active status?

To reactivate a license from Inactive to Active status, the licensee must complete 80 hours of technical continuing professional education (CPE) during the 24 months preceding the request for reactivation. This requirement aims to ensure that the licensee is up to date with current accounting practices and standards before resuming professional practice.

Is there a need to renew the certificate even if it's in Inactive status?

Yes, licensees must continue to renew their permanent certificate on a regular biennial basis, even if it is in Inactive status. Failure to renew can result in the expiration or revocation of the certificate, which may complicate the process of returning to Active status.

Are there any penalties for violating the terms of Inactive status?

Violation of the terms of Inactive status, including performing services for the public or improperly using professional titles, is cause for disciplinary action by the Tennessee State Board of Accountancy. This can include fines, additional educational requirements, or even revocation of the license, depending on the severity of the violation.

How is the form submitted to the Tennessee State Board of Accountancy?

The completed and notarized IN 1324 form must be submitted to the Tennessee State Board of Accountancy at their Nashville office. Licensees can deliver the form in person, via mail, or fax to the contact information provided on the form. It's important to ensure the form is fully completed and accurately notarized to avoid delays in processing the request for Inactive status.

Common mistakes

Filling out forms accurately is crucial, especially when it comes to regulatory matters like the Tennessee In 1324 form for Certified Public Accountants (CPAs) who wish to change their status to inactive. Here are six mistakes often made during this process, leading to unnecessary delays or issues:

Not providing complete information: A common error is leaving sections blank or providing incomplete responses. Every field, especially those requiring the licensee's full name, address, and certificate number, must be filled out thoroughly to avoid processing delays.

Incorrect dates: When stating the date since the licensee has not offered public accounting services, it’s vital to ensure accuracy. This date must precede the period for which the exemption is sought. Providing incorrect dates can misrepresent eligibility for inactive status.

Failing to notarize the form: The affidavit requires notarization to be considered valid. Skipping this step or improperly completing the notarization can result in the form being rejected.

Omitting the affidavit signature: Forgetting to sign the affidavit section of the Tennessee In 1324 form is a critical oversight. The affiant's signature is necessary to attest to the truthfulness of the provided information and the understanding of the form's implications.

Not understanding the requirements for reactivation: Individuals often overlook the details about what is required to return to active status. Before submitting the form, it's important to acknowledge and understand the commitment to complete 80 hours of technical Continuing Professional Education (CPE) within the 24 months prior to the reactivation request.

Ignoring the continuation of biennial renewal: Even when on inactive status, it's mandatory to renew the certificate biennially and pay the associated fees. Neglecting this can lead to issues in maintaining even the inactive status.

In summary, when changing one's CPA status to inactive in Tennessee with the In 1324 form, diligence in completing every section accurately and acknowledging all commitments and regulatory mandates is indispensable. Overlooking these obligations can hinder the process, leading to potential delays or complications in changing statuses.

Documents used along the form

When engaging with the Tennessee In 1324 form, which is an Affidavit for CPE Exemption and Inactive CPA/PA Status, applicants might require additional documents to support their application or to comply with related regulations. These documents can range from those providing personal information to those validating professional standing or historical record. Below is a detailed overview.

- Application for CPA Licensure: Required for individuals applying to become certified public accountants in Tennessee. This document captures personal information, educational background, and examination scores.

- Professional Ethics Exam Certificate: This certificate proves that the individual has passed the AICPA Professional Ethics Exam, a prerequisite for obtaining CPA licensure in many states, including Tennessee.

- Continuing Professional Education (CPE) Records: These records document the completion of continuing education requirements. Active CPAs must maintain CPE credits to renew their licenses, while this form signifies moving to an inactive status where CPE credits are not required.

- License Renewal Form: Used by current license holders to renew their CPA or PA license with the Tennessee State Board of Accountancy. It typically requires updating personal and professional information and paying a renewal fee.

- Reinstatement Application: Necessary for individuals looking to return to active status from an inactive status. It includes requirements such as proving the completion of CPE credits.

- Peer Review Compliance Form: Demonstrates that a CPA or CPA firm has undergone a peer review, which is a periodic external review of a firm's quality control system in accounting and auditing, as required for active practicing accountants.

- Character Reference Form: Used to provide evidence of good character, an essential requirement for CPA licensure. It typically requires signatures from colleagues or other professionals who can vouch for the applicant's integrity and professional behavior. Change of Address Form: Allows licensees to update their address details on file with the Tennessee State Board of Accountancy. Keeping this information current is crucial for receiving important communications.

- Notification of Name Change Document: Essential for updating the Tennessee State Board of Accountancy records in case of a legal name change, due to marriage, divorce, or other reasons.

- Tax Compliance Certification: Some states require proof of compliance with state tax laws for licensure. This document certifies that the individual is up to date on personal and business state tax obligations.

While the primary goal of the Tennessee In 1324 form is to shift from an active to an inactive status, thereby exempting the individual from certain professional engagements and continuing education credits, the additional documents listed provide vital support. They ensure continued compliance, facilitate record-keeping, and confirm the professional and ethical standing of accountants in Tennessee. For any CPA or PA navigating these processes, having these documents in order ensures a smoother transaction with the Tennessee State Board of Accountancy.

Similar forms

The Affidavit for Reinstatement to Active Status is one document that resembles the Tennessee IN 1324 form. This affidavit typically pertains to professionals who previously chose to become inactive but now wish to return to active practice. Similar to the IN 1324 form, it requires the professional to attest to their compliance with specific conditions laid out by their regulatory board, such as completing a defined amount of continuing professional education (CPE) prior to the reinstatement. Additionally, it must be notarized to verify the identity and acknowledgment of the signee.

Another similar document is the Continuing Professional Education (CPE) Reporting Form. This form is used by certified professionals to record and report their continuing education activities to their respective regulatory board. Although its primary purpose is different, it shares the concept of maintaining professional standards through education with the IN 1324 form. Both documents ensure that the professionals stay updated with the latest practices and regulations of their profession and require detailed information about the professional activities undertaken during a specified period.

The Professional License Renewal Form also shares similarities with the Tennessee IN 1324. This form is necessary for professionals looking to renew their license to practice within their field. Much like the IN 1324, it involves a state's regulatory body overseeing the licensing process and often requires the licensee to affirm that they have met certain conditions, such as completing requisite CPE hours or paying appropriate renewal fees. Also, it maintains the standard of professional conduct by enforcing compliance with the state’s legal requirements.

The Request for Change of License Status form is another document similar to the IN 1324. This form is used by licensees wishing to change their license status, such as from active to retired, or in the case of the IN 1324, from active to inactive. The form requires detailed personal and professional information from the licensee and an explanation for the request, including any compliance with the regulatory board’s requirements. It serves to officially document the licensee's intent and ensure that any change in status does not violate state regulations.

Lastly, the Certificate of Professional Conduct is akin to the IN 1324 form in that it often requires notarization and serves as an official statement of a professional’s status and compliance with regulatory standards. Typically issued by a professional's regulatory body, it verifies the professional’s standing and adherence to ethical or regulatory guidelines. While the Certificate of Professional Conduct is more about affirming current good standing, both it and the IN 1324 ensure that professionals meet the standards set forth by their regulatory boards and the law.

Dos and Don'ts

Filling out the Tennessee In 1324 form is an important process for certified public accountants (CPAs) or licensed public accountants (PAs) in Tennessee who wish to change their status to inactive and declare themselves exempt from Continuing Professional Education (CPE). To ensure this process goes smoothly, here are some essential do's and don'ts to keep in mind:

Do:- Read the instructions carefully before you start filling out the form. Understanding every part of the document is crucial to complete it correctly.

- Ensure that your full name and address are printed or typed clearly to avoid any misunderstandings or miscommunications.

- Be honest and accurate when providing the date since you last performed or offered to perform services involving accounting or auditing skills to the public. This information is critical for your affidavit.

- Sign and date the affidavit in the presence of a notary to validate your statements and intentions.

- Renew your permanent certificate on a biennial basis, even while in inactive status, to comply with the Board’s requirements.

- Leave any fields blank. If a section does not apply to you, consider marking it as ‘N/A’ rather than leaving it empty to show that you have acknowledged every part of the form.

- Use vague language when stating the services you have not performed. Clarity here can prevent potential legal or administrative issues.

- Forget to have the form notarized. Without notarization, your affidavit is not legally valid and will not be accepted by the Tennessee State Board of Accountancy.

- Assume that changing to an inactive status relieves you of all responsibilities. Remember, you must still renew your permanent certificate and pay any applicable fees, and you must meet the CPE requirements if you wish to reactivate your license.

By following these guidelines, you will navigate the process more smoothly and ensure your compliance with the requirements of the Tennessee State Board of Accountancy. Remember, the decision to change your professional status is significant, and compliance with all procedural requirements is critical for a successful transition.

Misconceptions

The Tennessee In 1324 form is critical for Certified Public Accountants (CPAs) and Public Accountants (PAs) in Tennessee who wish to change their status from active to inactive with the Tennessee State Board of Accountancy. However, there are several misconceptions regarding this form and its implications. Understanding these misconceptions is vital for accountants considering changing their status.

- Misconception 1: Filing the form terminates the need for CPE (Continuing Professional Education). While the form does grant an exemption from continuing education requirements during inactive status, returning to active status requires completion of 80 hours of technical CPE in the 24 months before reactivation.

- Misconception 2: The change to inactive status is irreversible. On the contrary, licensees can return to active status by completing the necessary CPE requirements and applying for reactivation with the Board of Accountancy.

- Misconception 3: Surrendering the right to practice public accountancy means you can no longer work in accounting. This is not accurate. It merely means you cannot offer public accountancy services to the public or use the CPA or PA title without stating 'Inactive.' Accountants in inactive status can still work in private sectors or non-public accounting roles.

- Misconception 4: Inactive status eliminates the need to renew the license. Even in inactive status, certificate holders must renew their certification biennially and pay the applicable renewal fees to the Board of Accountancy.

- Misconception 5: The affidavit for CPE exemption and inactive status does not need to be notarized. The form must indeed be notarized, as stated in its title and instructions, to verify the identity of the licensee and the authenticity of their declaration.

- Misconception 6: Once inactive, you cannot be disciplined for accounting practice violations. In reality, any violation of the Tennessee Code Annotated, Title 62, Chapter 1, and/or the rules and policies of the Board related to the practice of public accountancy can still result in disciplinary actions.

- Misconception 7: There is no deadline to apply for inactive status after ceasing public accountancy services. Correctly, the date you last provided public accountancy services must precede the period for which you are seeking exemption, implying timing is crucial when filing the form.

- Misconception 8: Any CPA or PA can file for inactive status without limitations. The right to change status is contingent on affirming you have not performed services requiring accounting or auditing skills for the public since a specified date, restricting eligibility to those who truly have not practiced as outlined.

- Misconception 9: Filing this form affects your standing with the IRS regarding tax preparation. The form only pertains to the Tennessee State Board of Accountancy. It does not impact your ability to prepare taxes unless you are presenting yourself as an active CPA or PA in doing so.

It's essential for CPAs and PAs in Tennessee to fully understand these points to make informed decisions about their licensure status and comply with state regulations.

Key takeaways

Filling out and using the Tennessee IN 1324 form is a significant step for certified public accountants (CPAs) or licensed public accountants (PAs) in Tennessee who wish to change their status to inactive. Below are key takeaways to remember:

- The IN 1324 form is specifically designed for CPAs or PAs in Tennessee wanting to transition from an active to an inactive status while not performing public accountancy services.

- By opting for an inactive status, licensees agree to surrender their right to practice public accountancy. This includes not performing services involving accounting or auditing skills, management advisory, financial advisory or consulting services, and preparing tax returns or providing advice on tax matters.

- It's crucial to ensure the affidavit is notarized to confirm the authenticity of the licensee's declaration.

- The licensee must clearly indicate they understand switching to an inactive status means they cannot use the title of CPA or PA without including 'Inactive' adjacent to it.

- Understanding and agreeing to continue renewing the permanent certificate on a regular biennial basis, along with paying the necessary renewal fees, is mandatory even in inactive status.

- To return to active status, the licensee must complete eighty (80) hours of technical Continuing Professional Education (CPE) during the 24 months preceding the date they request reactivation.

- Violating the Tennessee Code Annotated, Title 62, Chapter 1, or the rules and policies of the Tennessee State Board of Accountancy may lead to disciplinary action.

- It is emphasized that the licensee should have a thorough understanding of the Law and Rules of the Board of Accountancy before submitting the form.

It is essential for licensees to review these points carefully to ensure compliance with the requirements laid out by the Tennessee State Board of Accountancy when making a transition to an inactive status. This will help avoid any potential issues or misunderstandings in the process.

Popular PDF Forms

Tennessee Articles of Organization - Ensure your Tennessee LLC kicks off without a hitch by accurately completing the Articles of Organization form.

Tennessee Ps 0376 - Companies employing advanced dialing technology in Tennessee must disclose this in the application.